The Two Lammert Time-Based Fractal Laws of Self-Assembly:

A 4-Phase Series: x/2-2.5x/2-2.5x/1.5-1.6x , where the 3rd fractal ends on a peak or lower high valuation and the other 3 Fractals end on nadir valuations.

A 3-Phase Series: x/2-2.5x/1.5-2.5x, where all 3 fractals end on nadir valuations. This can be written as y/2-2.5y/2-2.5y for crash devaluations where ‘y’ denotes declining valuations.

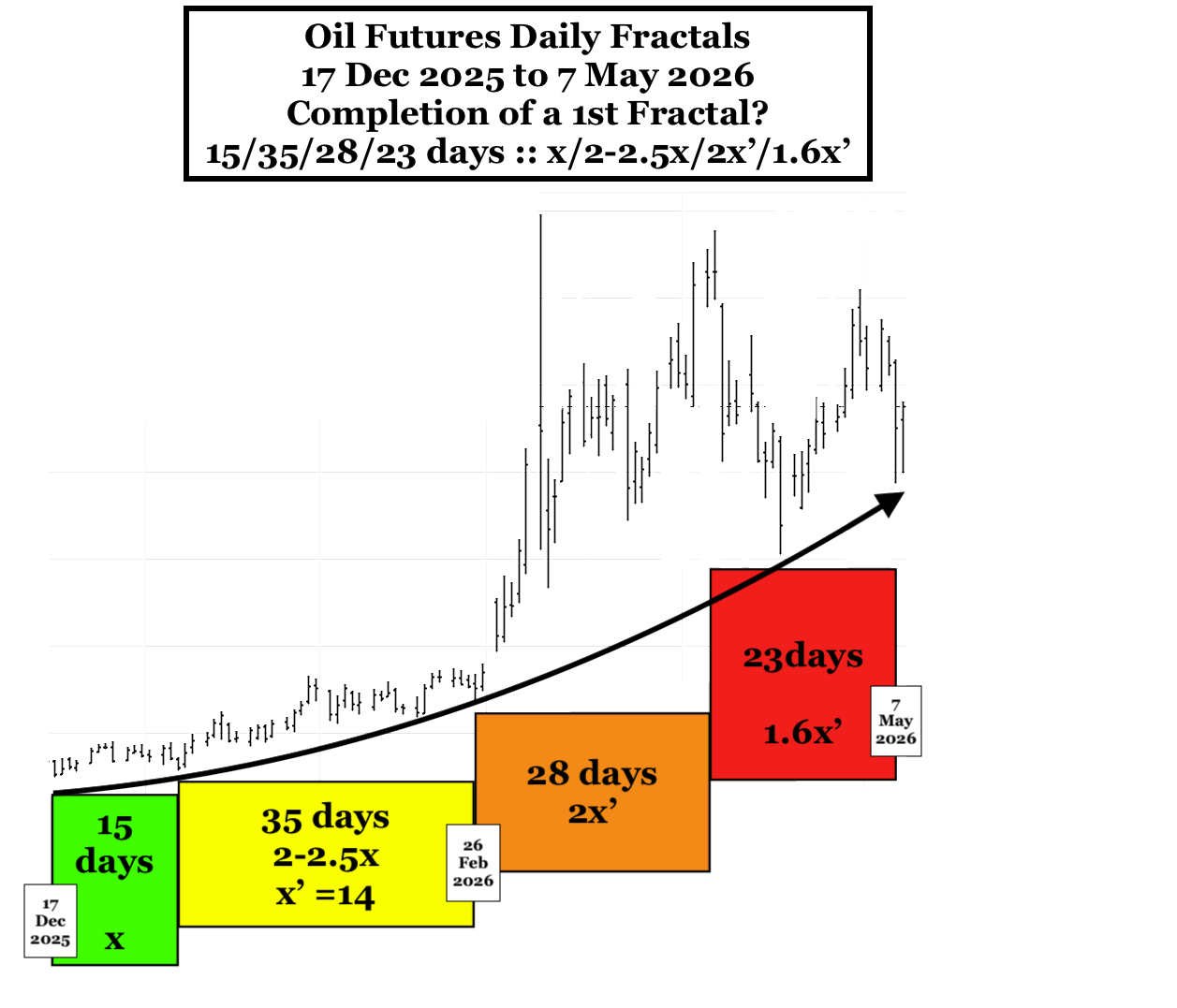

(Added 7 May 2026) Or very ominously, completion of a 16 Dec 2025 to 7 May 2026 15/35/28/23 day :: x/2-2.5x/2x’/1.6x’ 1st Fractal with a curvilinear underlying tangent line signalling explosive 2nd Fractal valuation growth. The war on the 28 February 2026 was the start of accelerating 28 day 3rd fractal subseries growth.

2% US GDP growth and US Equity valuation growth in the 1st quarter and the 1st month of the 2nd quarter has been propelled by continued private credit investment into AI and associated Tech, while the US consumer dromedary economy is faltering as represented by historically low consumer sentiment and the added gas and diesel price increase straws that are breaking the camel’s back.

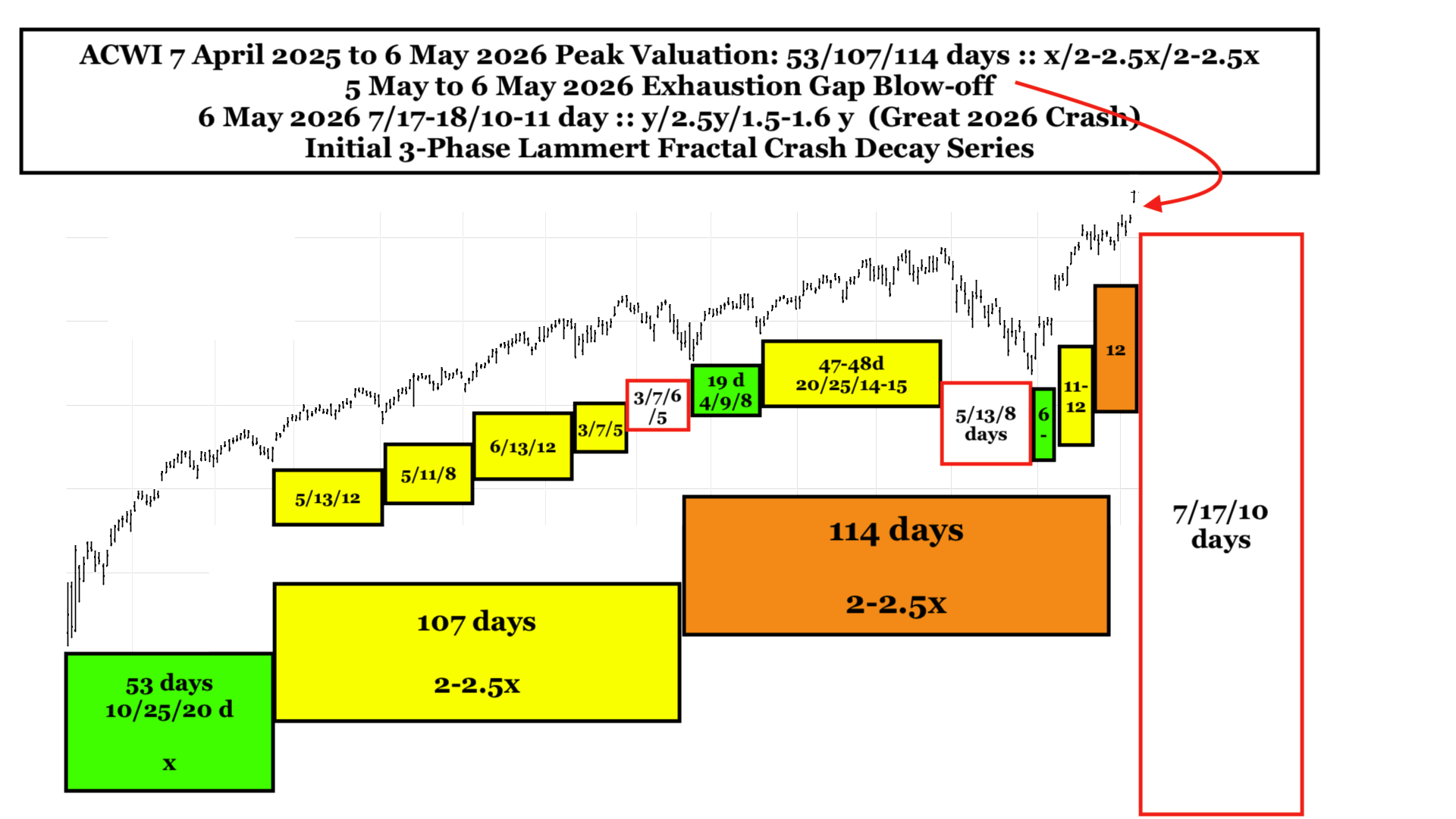

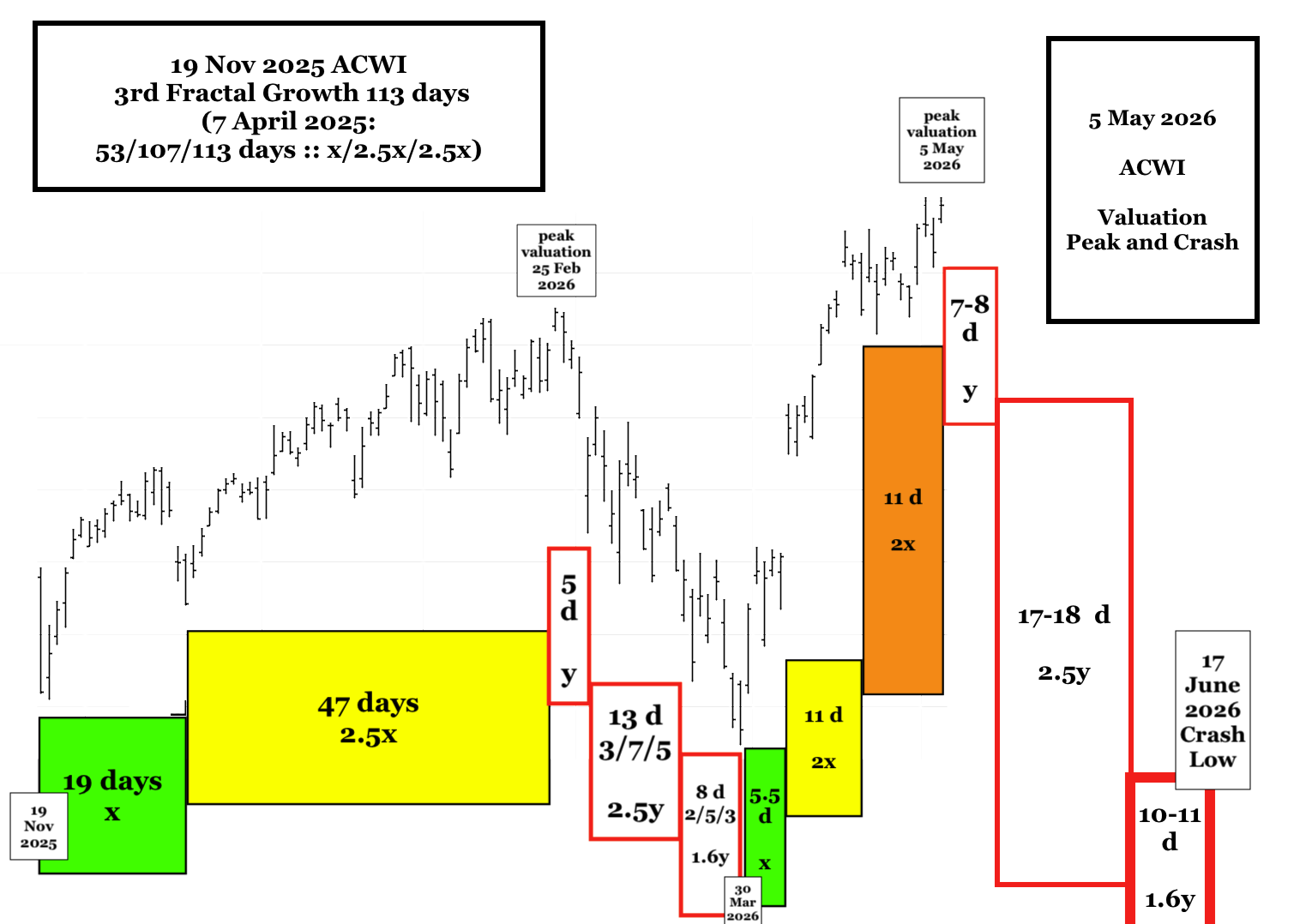

After ACWI’s 7 April 53/107 day 2nd Fractal valuation nadir on 19 Nov 2025, ACWI valuation growth occurred in a 19/47 day :: x/2.5x fractal fashion with an initial peak valuation on 25 Feb 2025. From the 25 Feb 2026 peak ACWI fractal decay occurred in y/2.5y/1.6y fractal series fashion: 5/13/8 days ending on 30 March 2026. The fractal collapse occurred coincidentally to the start of the Israeli-US war.

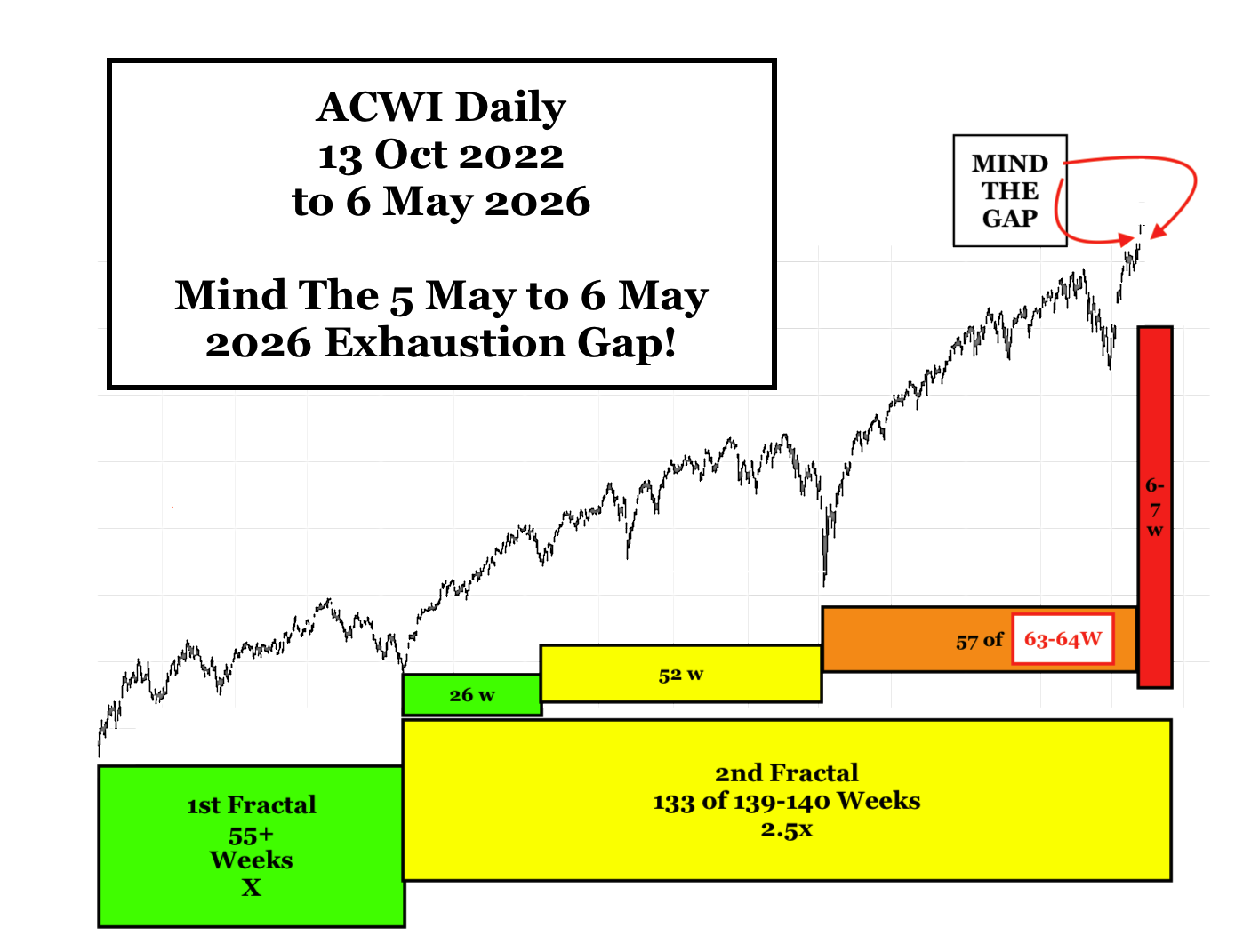

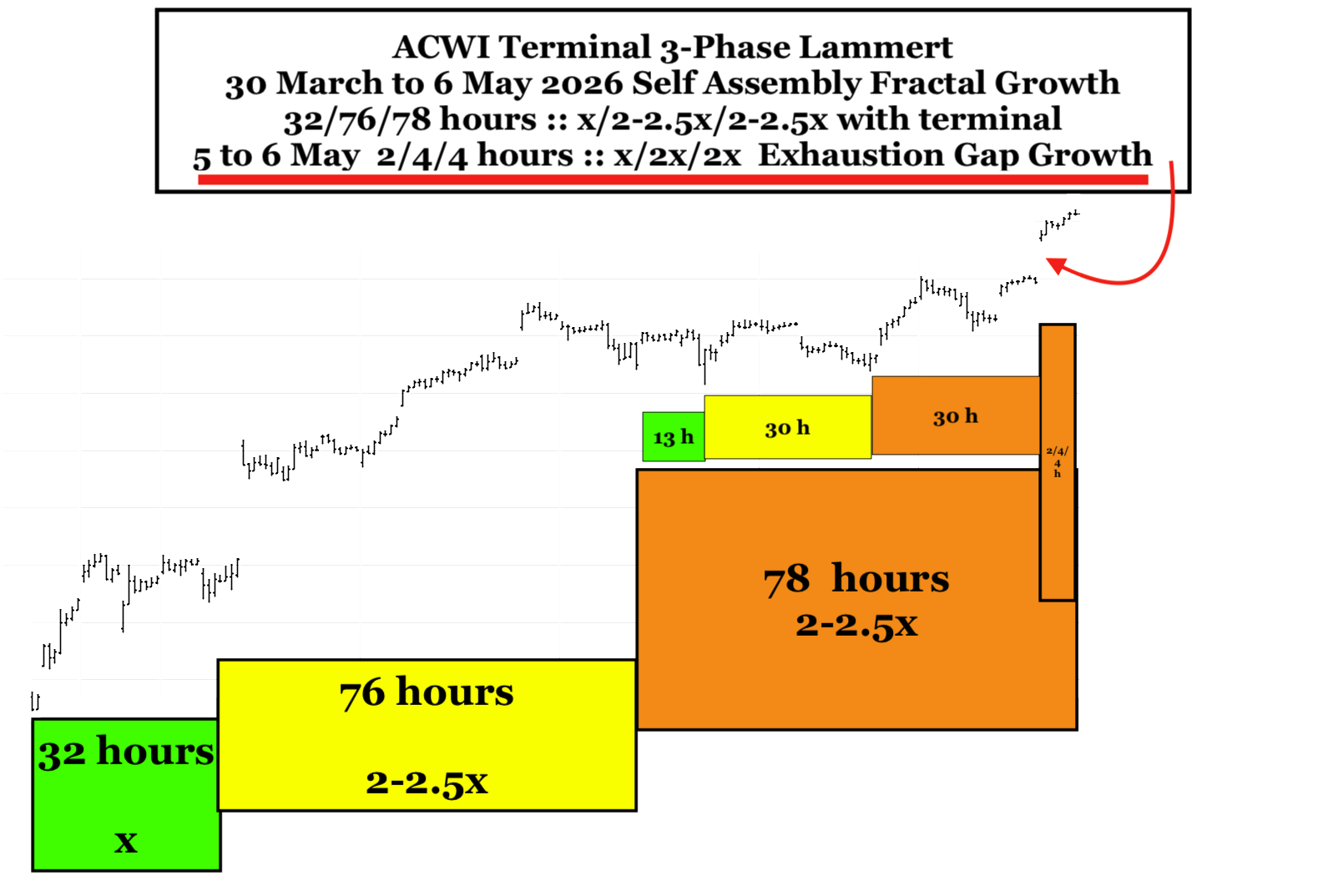

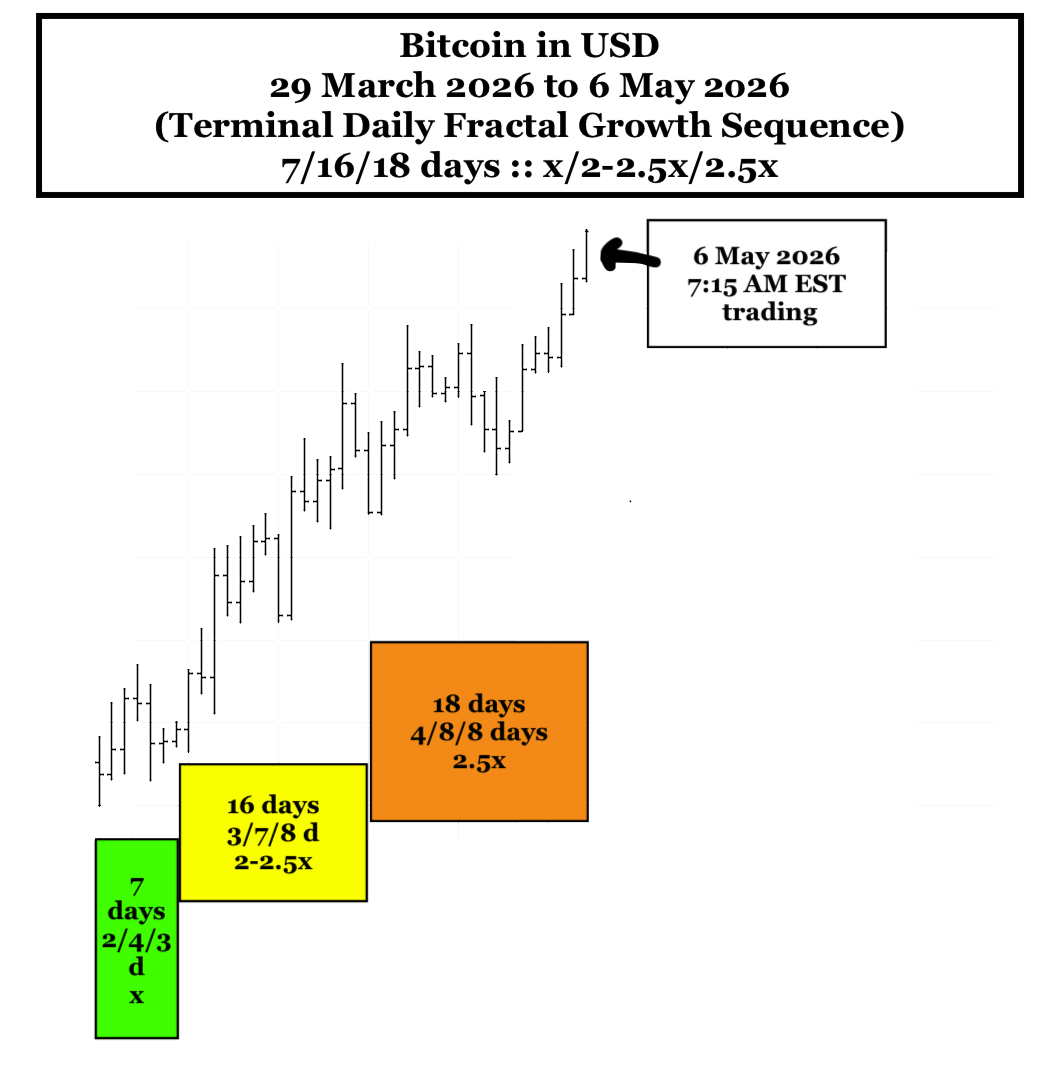

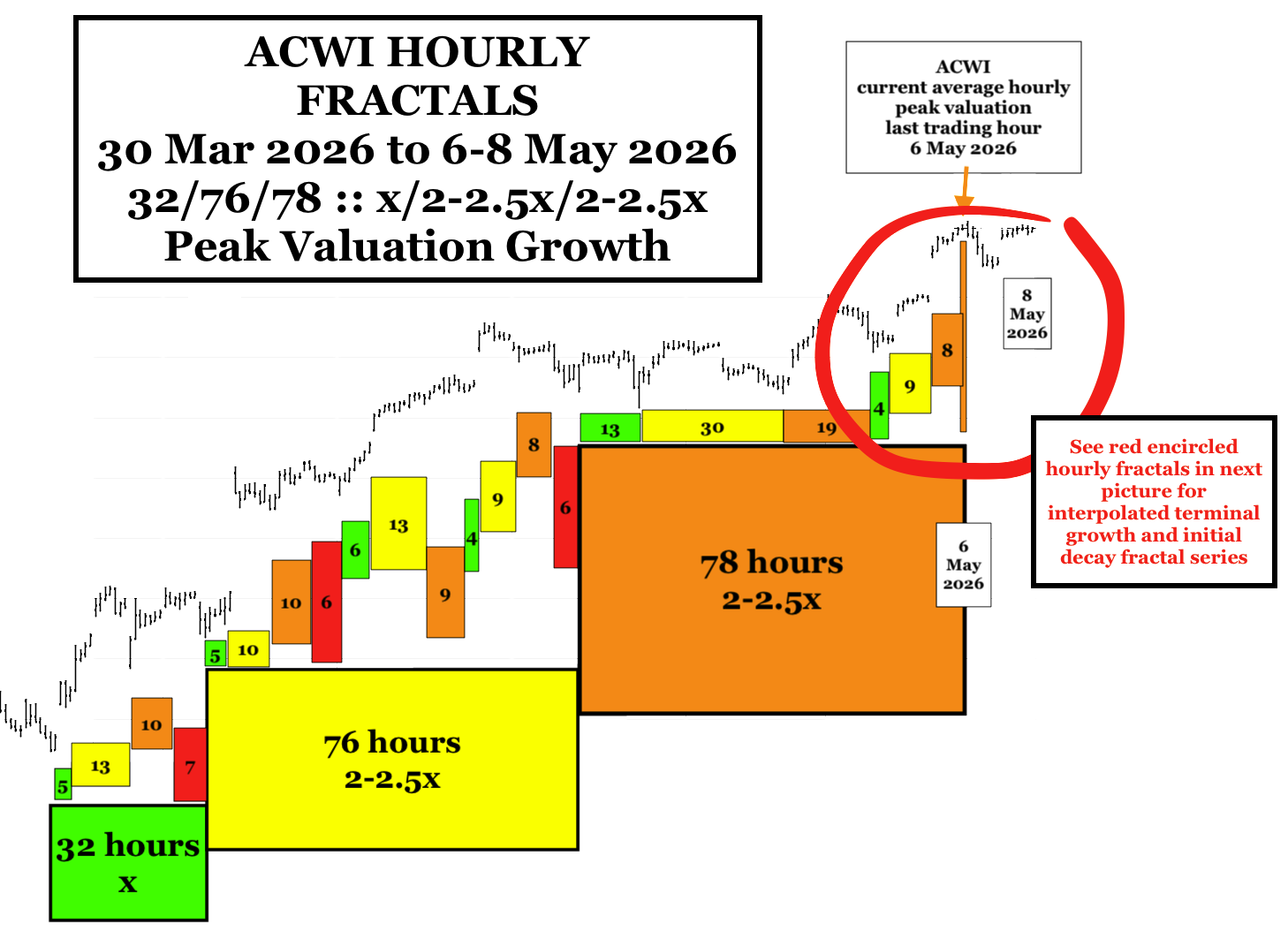

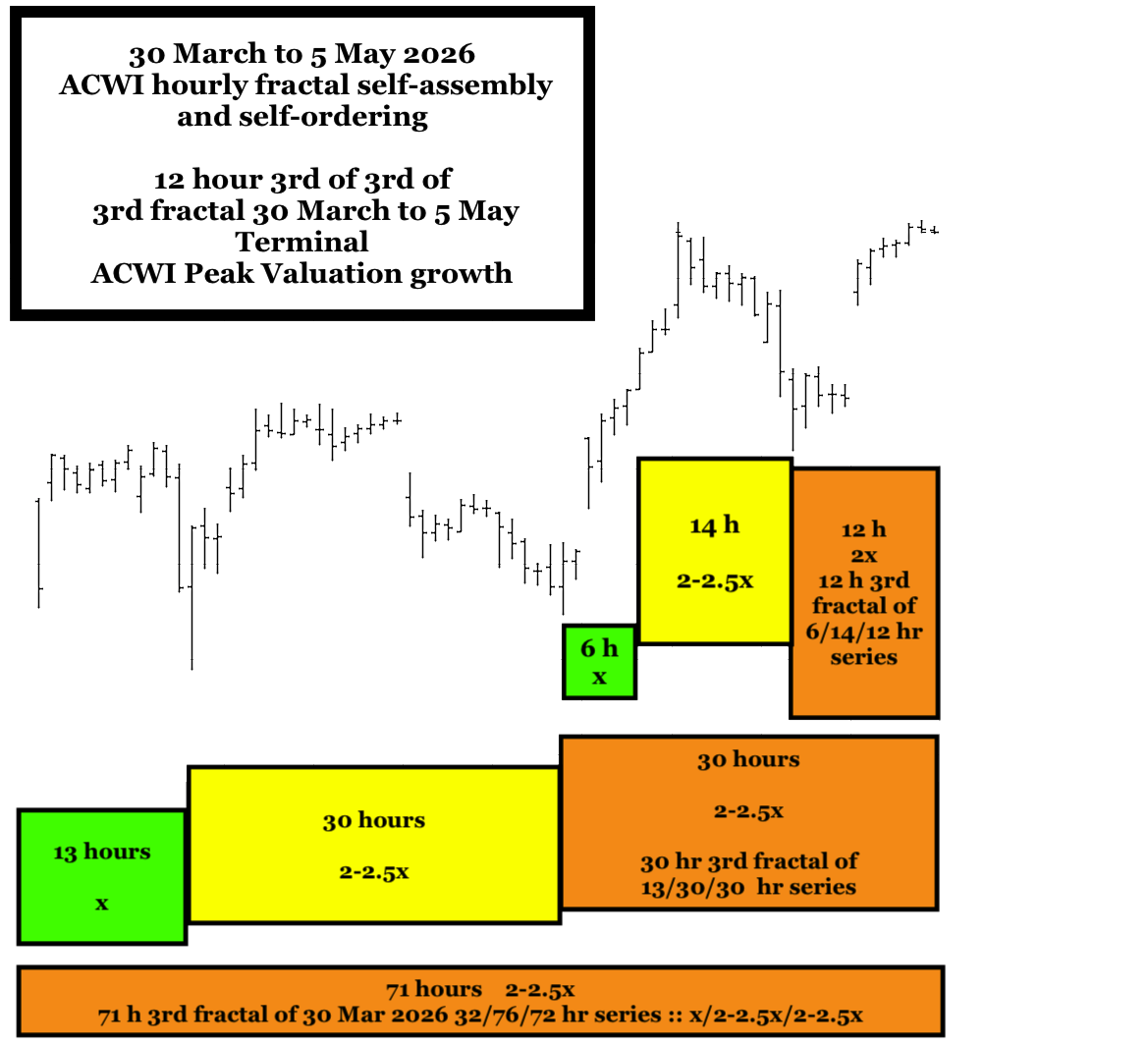

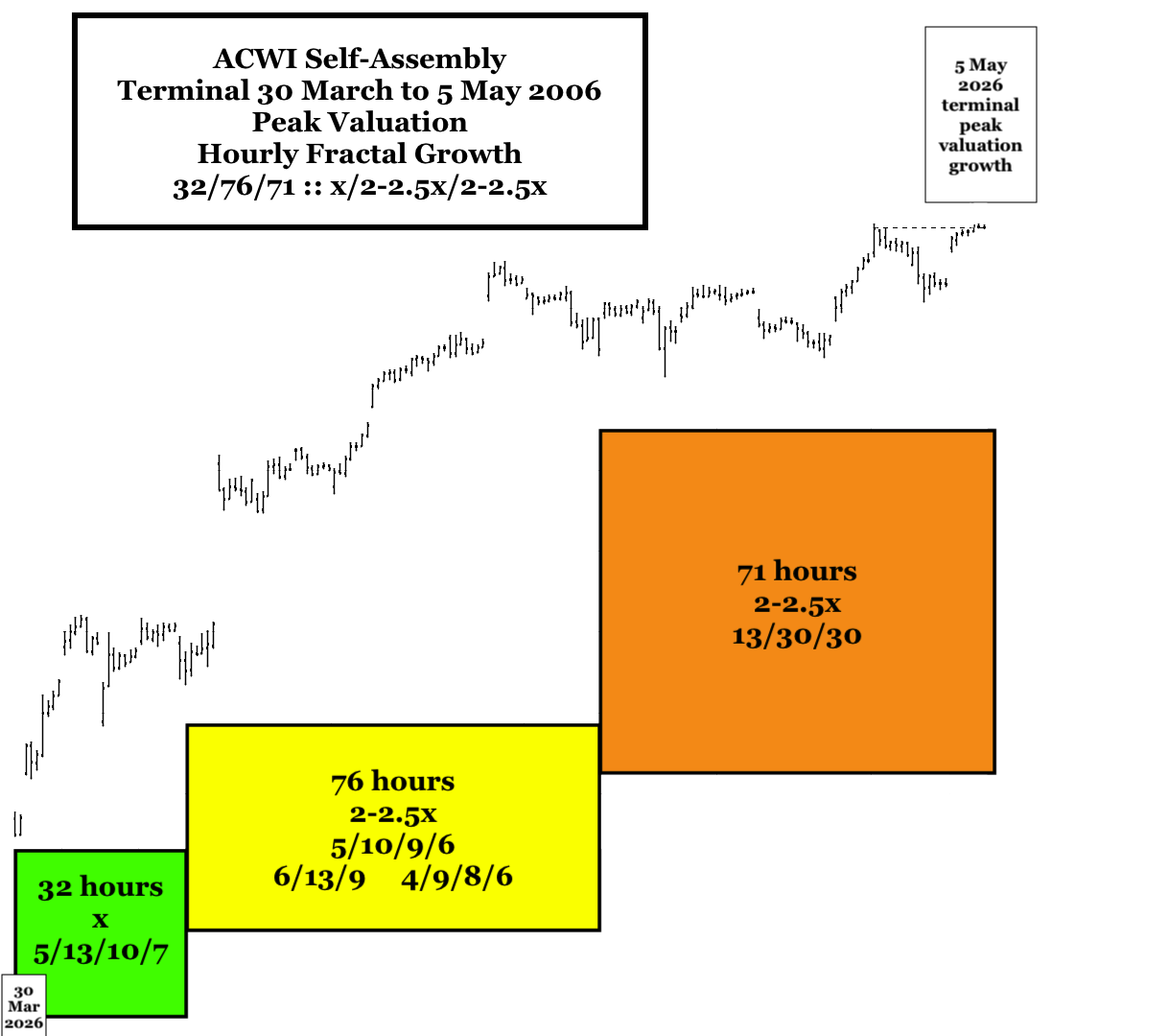

30 March to 5 May 2026 represented the global asset-debt macroeconomic system’s terminal fractal x/2-2.5/2-2.5x growth. 5 May 2026 was the ACWI Global Peak Valuation of the 1982 SPX 13/33 year :: x/2.5x 1st and 2nd fractal series. Final daily and hourly growth for ACWI started on 30 Mar 2026 and followed a 6-/11/11 day :: x/2x/2x terminal growth series and a 32/76/71 hour growth series :: x/2-2.5x/2-2.5x ending with a lower interday high on the last trading hour of 5 May.

The last trading hour of 5 May completed a 12 hour 3rd fractal of a 6/14/12 hour 3 phase fractal series of 30 hours the sum which completed the 3rd fractal of a 13/30/30 hour fractal series, the sum which completed a 71 hour 3rd fractal of a 30 March 2026 32/76/71 hour fractal series.

The daily and hourly series completes a 7 April 2025 53/107/113 days :: x/2-2.5x/2-2.5x approximating x/2x/2x.

The 53/107/113 or 270 day 3-phase series completes a 23 Oct 2023 120/243/270 day :: x/2-2.5x/2-2.5x fractal growth series.

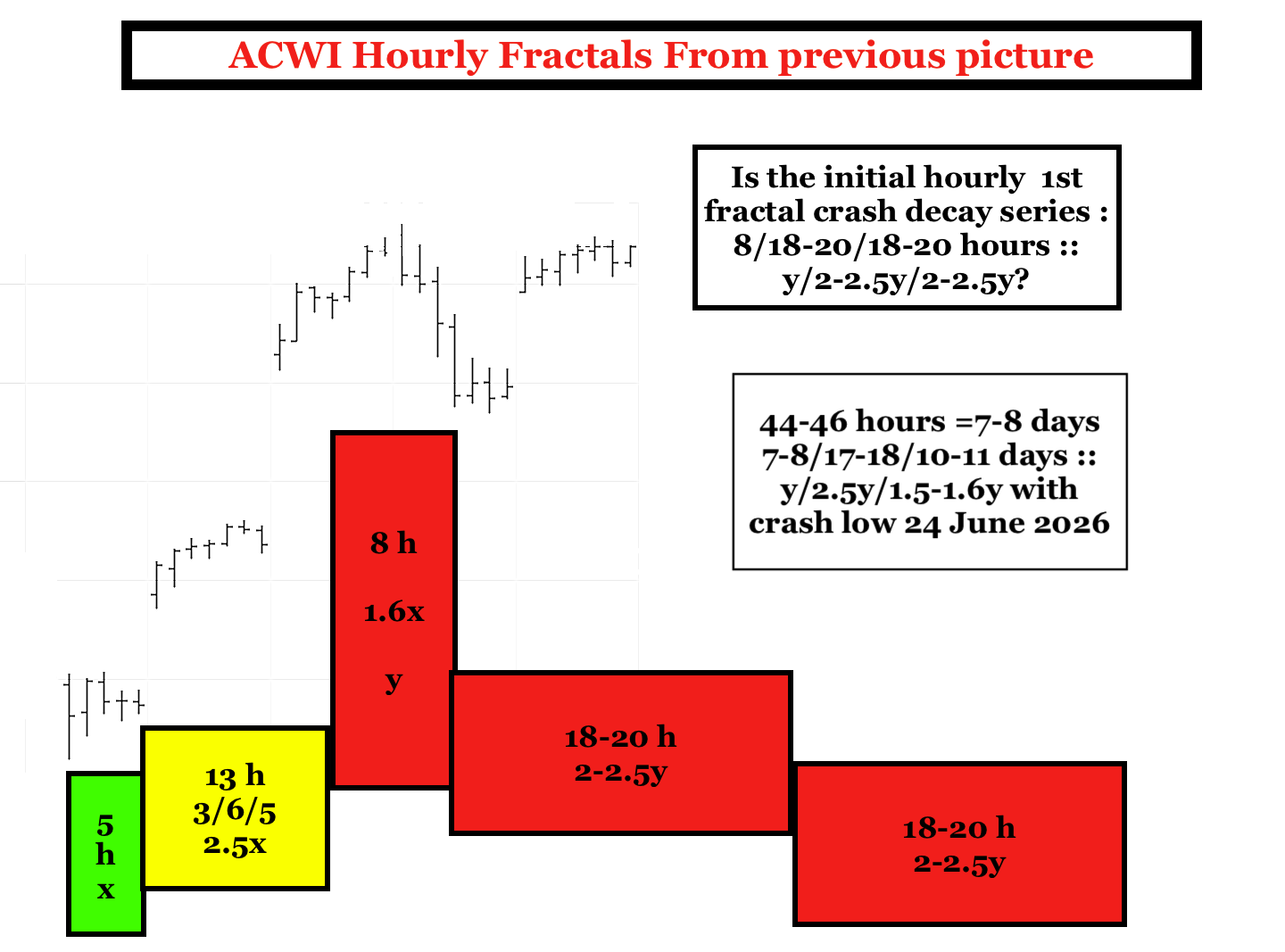

A 5 May 2026 7-8 /17-18/10-11 day :: y/2-2.5y/1.6y 3-phase crash decay series ending about 17 June 2026 will complete a 23 Oct 2023 120/243/305 day :: xy/2-2.5xy/2-2.5y 3-phase growth and decay series and a Oct 2022 55+/140 week :: x/2.5x 1st and 2nd fractal series.

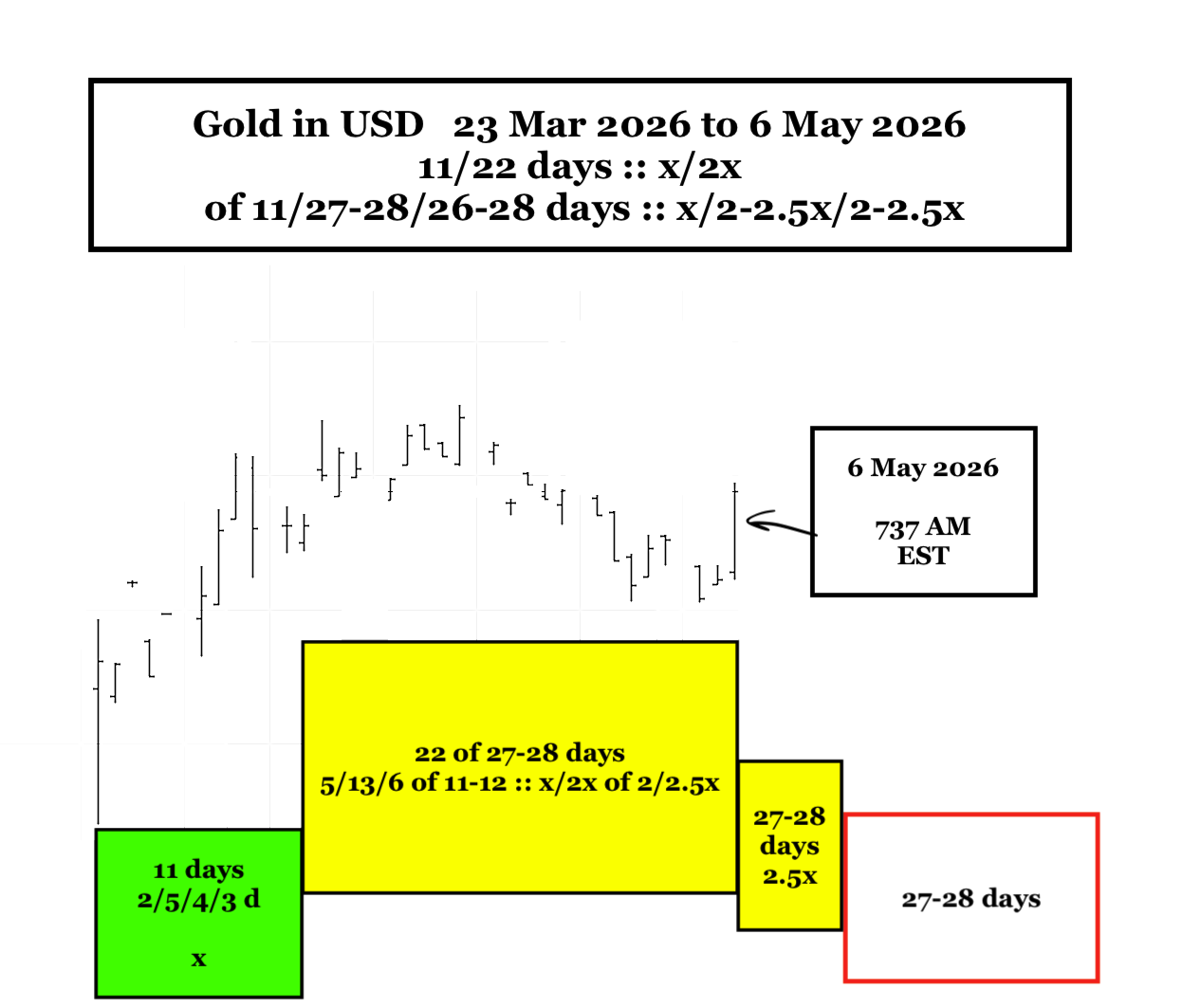

GOLD Gold prices appear to be following a 1929 DJIA 3 phase 11/27-28/27-28 day: xy/2.5xy/2.5xy 3-phase crash fractal decay series. The 11 day 1st fractal started on 23 March 2026.

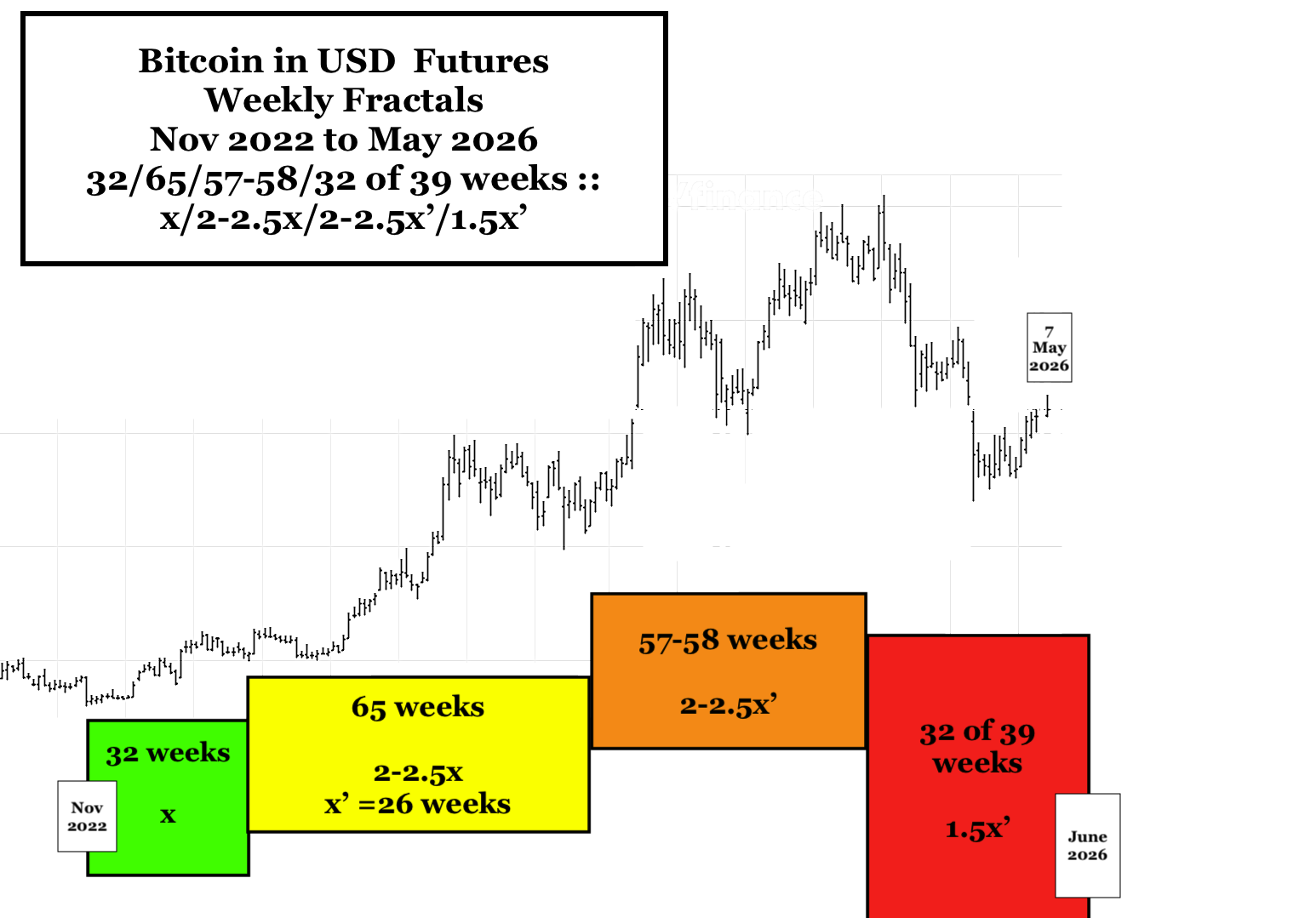

CRYPTO is following a 12 Dec 2022 26/66/56-57/31 of 38-39 week :: x/2.5x/2-2.5x/1.5x 4-phase growth and decay fractal series.

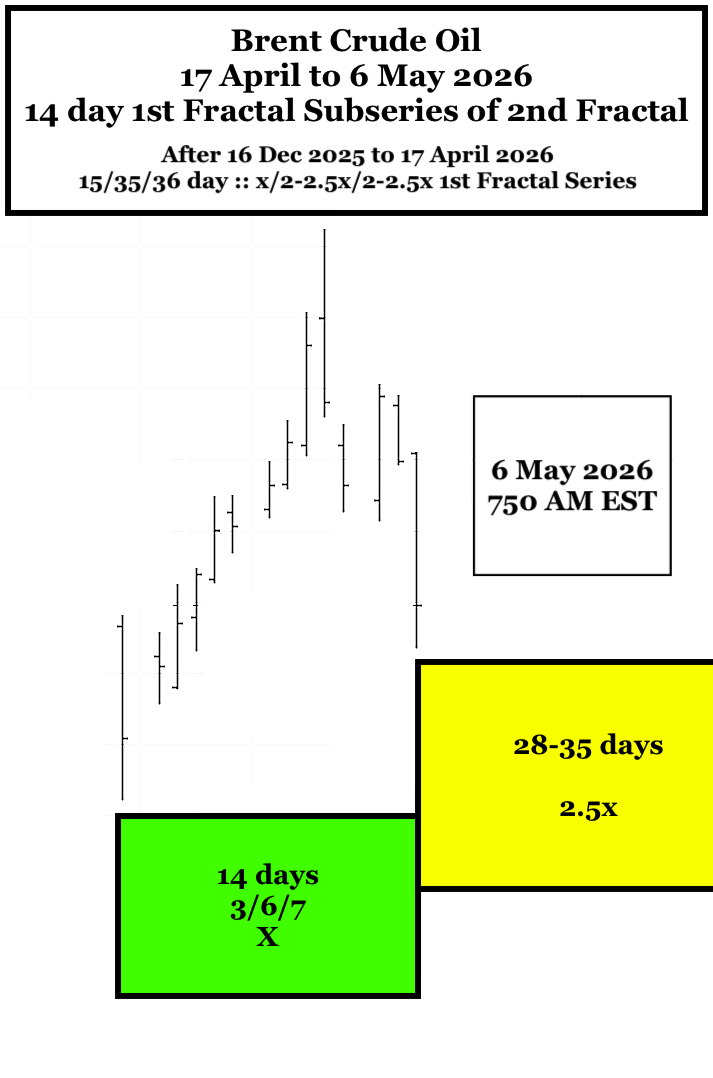

OIL With the war, oil is bucking the trend having completed a 16 Dec 2025 15/35/36 day 1st fractal growth series on 17 April 2026. On 4 May 2026 the 2nd fractal appears to be on day 12 of a 12 day 1st fractal sub-series. On 4 May 2026 the 2nd fractal appears to be on day 12 of a 12 day 2/5/5/3 day 1st fractal sub-series. Like the 25 Feb ACWI and ensuing 5/13/8 day collapse after the start of the war, accelerating oil and gas prices due to the continued Hormuz closure will be primarily blamed for the 5 May 2026 7-8/18/11 day :: y/2.5y/1.6y global equity crash and gold and crypto crash.

It is the opinion of this observer that the equity, gold, and crypto crash beginning 5 May 2026 is related primarily to private and zombie corporate credit excessive issuance for overvalued assets and the ongoing collapse of that private and corporate debt credit worthiness. The macroeconomic asset-debt system’s asset valuations (except oil and petroleum by-products) will undergo an inevitable 5 May 2026 peak valuation deterministic time-based fractal collapse.