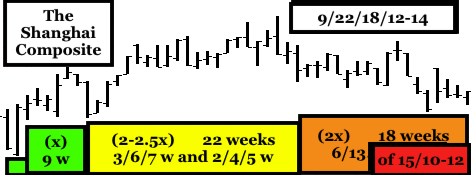

Last week completed a 9/22/18 week :: x/2-5x/2x 3 phase growth fractal series for the Shanghai Composite, exactly matching the Shanghai Property index: 9/21/18 weeks :: x/2-2.5x/2x. For the Shanghai property series this is subfractal 3 of a 5/12/12 of 13 month or a 5/12/10/3 of 7 month series. The Shanghai composite is following a March 2020 monthly 8/19/18 of 19-20 three phase fractal series or a 8/19/16/3 of 12 monthly four phase fractal series.

The March 2020 Shanghai Composite monthly fractal series matches numerically the Wilshire composite’s,

Both composites have a 2/4/4 or 8 month subfractal 1 base.

Subfractal 2 of 19 months for the Shanghai consists of two series: a 2/5/5 monthly series followed by a 2/4/4/3 monthly series. The Wilshire composite’s19 month subfractal 2 consists of a 4/9/10 month fractal series.

Subfractal 3 for the Wilshire consists of a reflexive decay and growth series 2/5/5/3 series and ends at month 16 with two weekly growth series a 2/5/5/3 weeks series [[12 weeks]] followed by a 2/5/5 week series (10 weeks).

An interpolated fractal series of [[12]]/28-30/28-30 weeks would complete a March 2020 8/19/16/12 month fractal series.

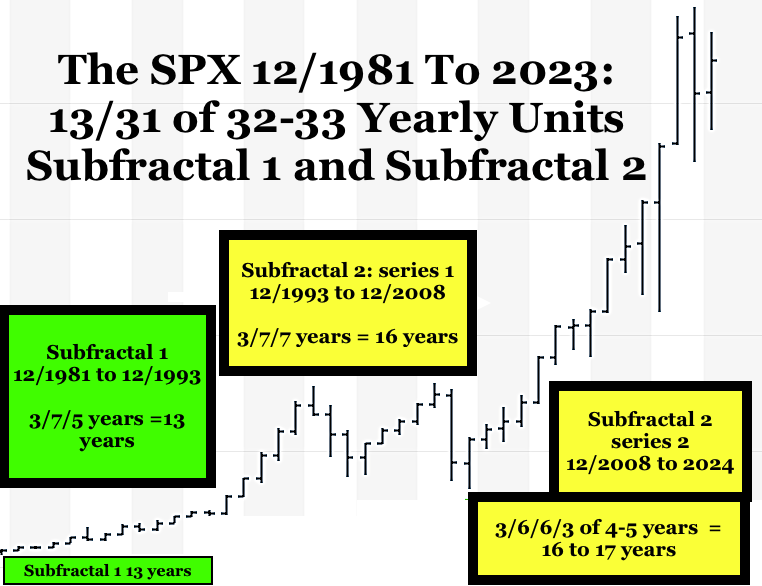

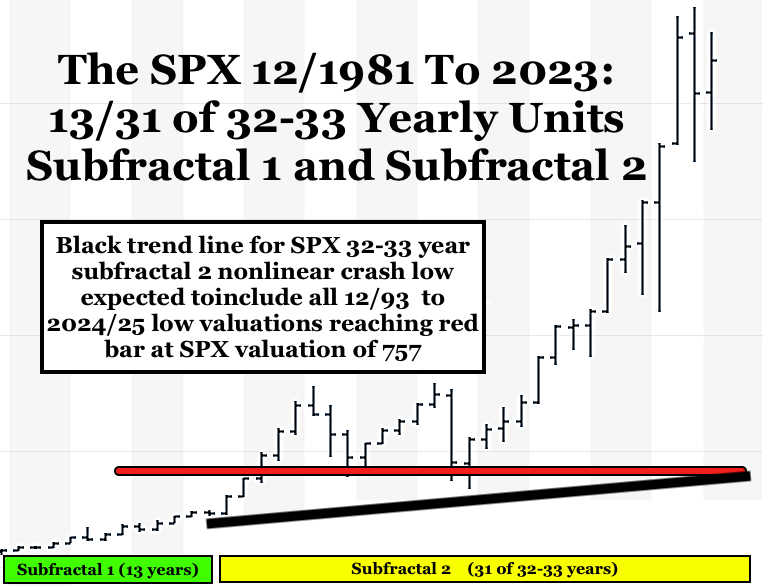

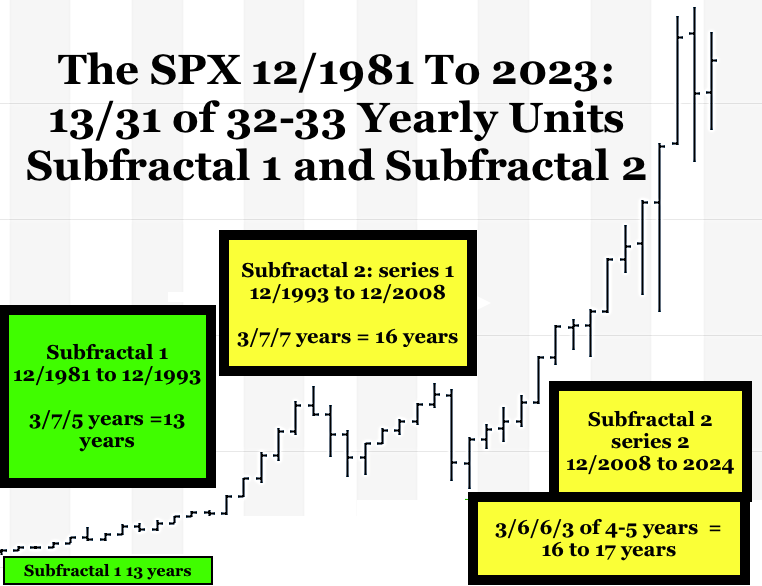

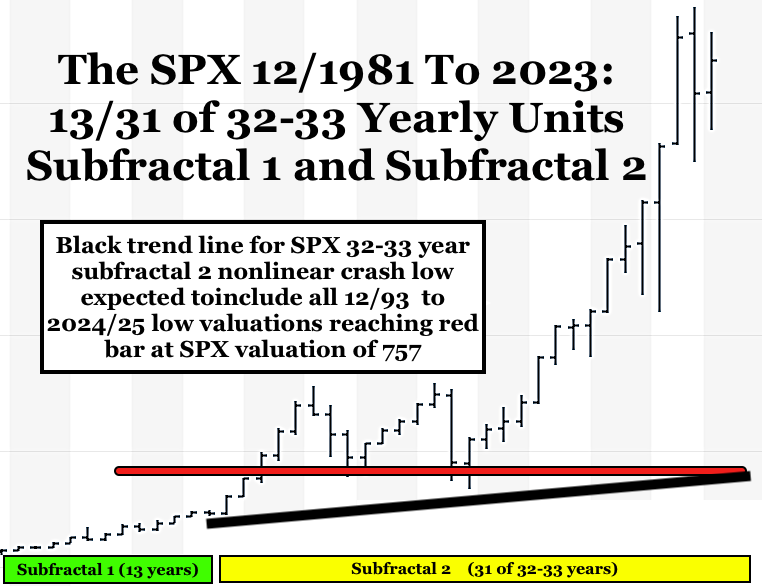

The global asset valuation collapse (including real estate prices)- propelled to extreme valuation heights by historical increases in liquidity, money expansion, and personal, corporate, and governmental debt expansion via low interest rate easy credit and central bank augmented residential and corporate loans – will take the Wilshire and SPX back to their 31 year 1993-4 to 2023-2025 trend line of a 1981-1982 subfractal one (13 years) and subfractal two (31 year) series.

Monthly September 2014 Bitcoin Fractal Series and Recent 9 March 2020 Monthly Ten Year Note Fractal series in the Asset Debt QE/QT 21st Century Macroeconomic System and in the Longer US Hegemony 19th century 1807 36/90/90/54 Year 4 Phase Lammert Fractal Series.

I. Current Monthly Model for the Wilshire March 2020 low fractal series: 8/20/16/12 months :: x/2.5x/2x/1.5x.

II. For System Simple Fractal laws, see 31 August 2023 section on A Primer on Fractal Series.

The Wilshire 13 August 2023 52/130/130 day fractal series mathematical model still holds with an 18 August 2023 6/15/4 of 15 day low on 5 October 2023 and further low near the end of November 2023 completing the 130 day subfractal 2.

Ten Year Note interest rates likely reached a peak yesterday rising from 0.4 % on 9 March 2020 to 4.62 % on 19 Sept 2023, a relative increase of 1150 %. From the 9 March 2020 low the ten year note followed a 7/16/17 month fractal growth series followed by a 5/11/10 week fractal growth series of 21/52/44 days.

Money exiting from stocks will drive interest rates lower.

Bitcoin in USD, traded 7 days a week, is following a 17 August 5/11/11 day fractal series followed by a 10 September 5/5 of 11/11 day series ending on 5 October.

The long term Bitcoin in USD monthly fractal series starting in Sept 2014 began as a complex initiating fractal series of (2)/4/8/6 months ending in January 2016. Why initiating? The trading market was just beginning with the Jan 2016 low valuation was below the initial Sept 2014 low. The last 6 months of this complex 17 month series served as an initiating base fractal (6 months) for a 15 month subfractal 1 of a 15/37/33 month series ending in November 2022. A 22 month lower low would complete a 15/37/33/22 month 4 phase fractal series. For the 22 months a November 2022 3/6/4 of 6 month series ending in November 2023 could be followed by a 2/5/5 month series ending in August 2024 to complete a self-assembled four phase Jan 2016 15/37/33/22 month :: x/2.5x/2-2.5x/1.5x fractal series.

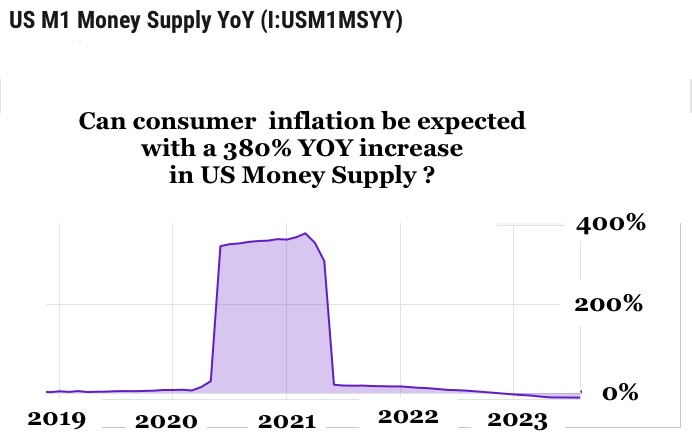

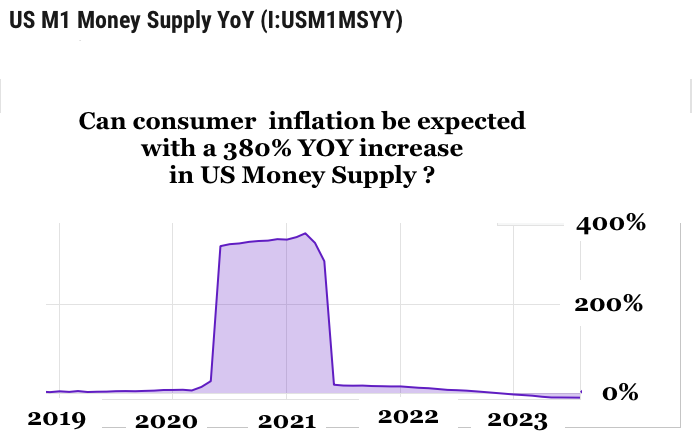

With residential and equity assets inflated and with easy loose money lending created by a 380%-460% one year M1 money supply increase from Feb 2020 to April 2021, a very hard deleveraging landing is expected with the completion of an composite equity 12/1981 to 8/2024 13/32 year :: x/2-2.5x subfractal 1 and subfractal 2 fractal series and an expected 32 year subfractal 2 trend line low valuation of 750 to 800 value on the SPX.

Nonlinearity for the asset debt macroeconomic system is a sudden daily, weekly, monthly, yearly mathematical fractal collapse of asset prices and zombie enterprises whose valuation growth and sustainability are based on prior easy credit, expansion of the money supply, and resulting gross overvaluation.

With the US’s winning of WW2(without destruction of its infrastructure), its resulting position as the global reserve currency, and its renewed uncoupling to a gold standard on 15 August 1971 (the Nixon shock), the US has been able to cascadingly expand its money supply via money printing and debt creation with a series of (fractal) asset price collapses with nadirs in Sept-Oct 1974, 19 October 1987, July and October 2002, March 2009, 6 May 2010 and March 2020.

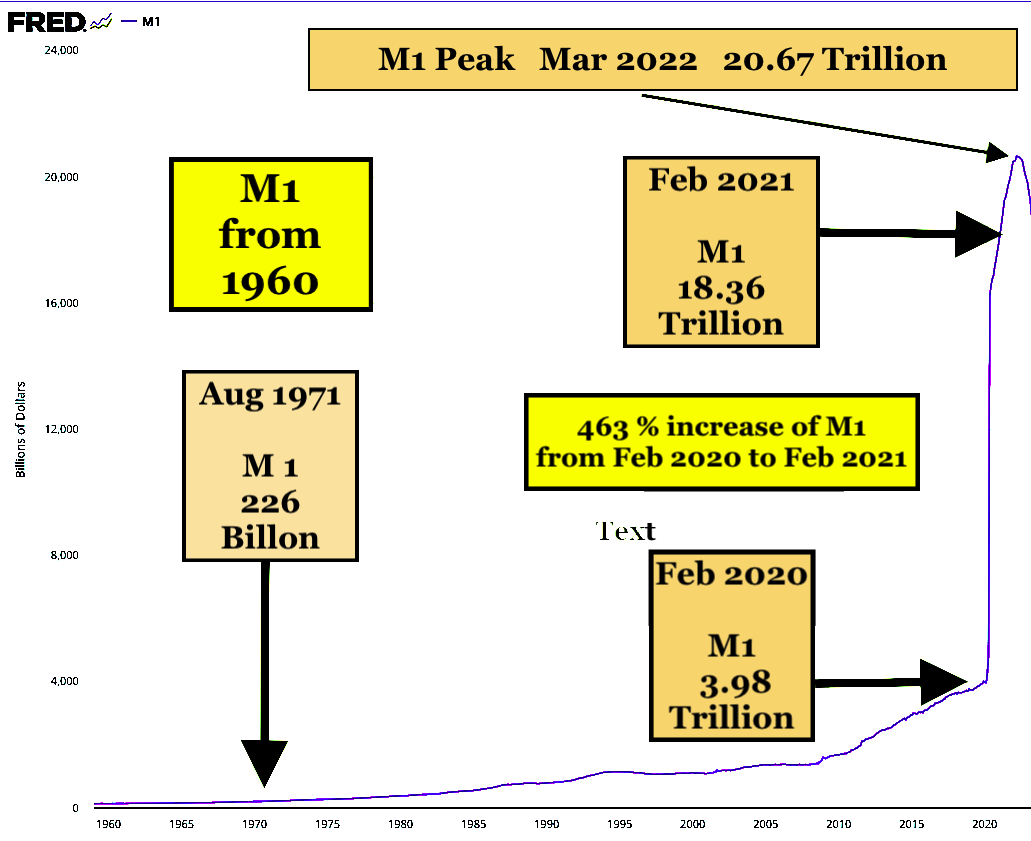

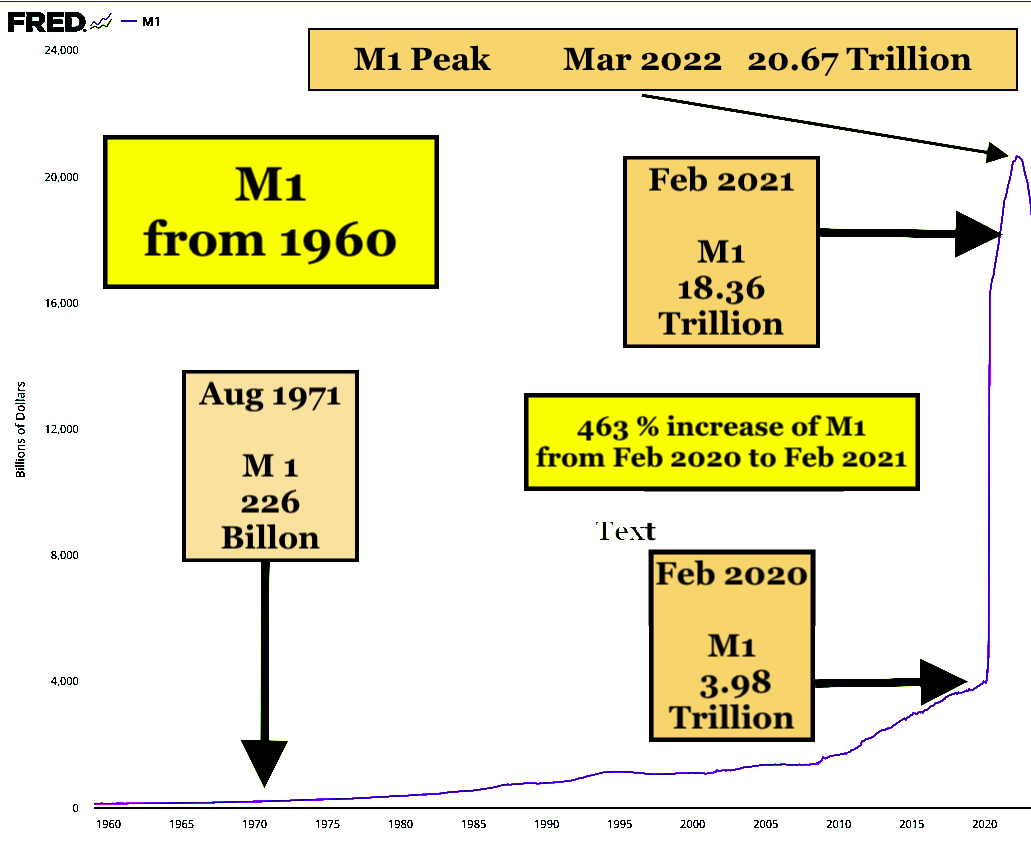

The M1 money supply.

The US money supply in 1929 was 26.5 billion and decreased to 19 billion in 1932, a drop of 28%.

From 1929(26.5B), the money supply increased to 226.5 billion in August 1971, an increase of 855% and an average increase of 20 % per year over the 42 year interim. After the Nixon Shock of decoupling from the gold standard in 1971, the US money supply increased from 226.5 billion to 3.97 trillion in Feb 2020, a 1766% increase over 49 years or an average of 36% per year.

The ‘Trump Shock’ and Covid occurred in 2020 with an increase in the US Money supply from February 2020 at 3.98 trillion to February 2021 to 18.36 trillion, a 463% increase in the money supply in single year (as compared to the prior average annual increase of 20 % and 36% in years before and after the Nixon Shock.)

The primary cause of US inflation was this one year 463 % increase in the US money supply sustained by the 2023 8-9 % COLA increase in social security payments for the 64 million + retired and disabled US citizens.)

M1 Money supply peaked at 20.7 trillion in March 2022 and has since decreased via QT and higher interest rates to about 18.4 trillion, a ten percent decrease over 15 months and beginning to rival the monthly average decrease % rate of the 1929 to 1932 M1 collapse. With a coming nonlinearity in asset prices, the decrease in money supply could exceed that of the decline during the 1929 to 1932 nadir.

The Federal reserve has predicted that post pandemic reserve savings for US citizens starting at 2.1 trillion in 2021(23 months ago) will reach zero by October 2023. https://www.youtube.com/watch?v=MQSgLJfsepA

What macroeconomically to the asset-debt system will happen after such extraordinary central bank QE/QT policies?

The current mathematical monthly decay fractal model for the Bank of Shanghai is a November 2017 9/20/18 month x/2-2x/2x 3 phase decline followed by a July 2021 3 phase decay decline of 9/19 of 20/12-18 months :: x/2-2.5x/1.5-2x.

For the Wilshire the asset valuation growth (QE) and (QT) decay model is a 4 phase March 2020 8/18-20/18-16/12- 13 month decay fractal series.

Fractal groupings are determined by trend lines connecting the lowest valuation of day one of the fractal series to the lowest valuation of the last day of the fractal series.

For the composite Wilshire a base fractal (subfractal 1) of 52 days is observable from the low on 13 Aug 2023 to 24 May.

Subfractal 2 is potentially composed of a x/2-2.5x/ 1.5x’ a three phase decay series; x’ = 2-2.5x divided by 2.5.

x is observable as 30 days from 24 May to 10 July. 2-2.5x is potentially 63 days, a 10/21/20/15 day series ending 5 Oct 2023. Subfractal 3 (1.5x’) is potentially a 37-38 day series. 63 divided by 2.5 equals 25 days times 1.5 equals 37-38 days ending 27/28 November.

27/28 November could represent a double bottom and serve as the base fractal for a 38/80/48 day :: x/2-2.5 x/1.5x’ series and completing a March 2020 33/72-73/72-73/44-45 week :: x/2-2.5x/2.5x’/1.5x’ 4 phase series.

The peak decay fractal series from 31 July starts on 27 July and consists of subfractal one: 3/7/6/4 days, or 17 day, a base for a 3 phase decay fractal series. (Note the downward trend line connecting the lows of 27 July and 18 Aug with all intervening days above the trend line.

Subfractal 2 appears to be a 34 day 6/11 of 15/15 day (three phase) fractal (decay series)ending 5 October.

Subfractal 3 of 37-38 days ending 27-28 November would complete a 13 August 52/128-129 day :: x/2.5x subfractal one and subfractal two series.

From 27 July 2023 the 3 phase decay series would be 17/34/37 days :: x/2x/2-2.5x.

An advantageous characteristic about fractal mathematical models is that a working model can be quickly determined to be wrong. The above model is consistent with empirically derived and observable simple laws of time-based fractal asset valuation growth and decay http://www.economicfractalist.com/blog/ (see 31 August posting) which appear to quantitatively govern asset growth and decay valuation pathways – qualitatively created more and more since late 2008 by historically extreme central bank cyclical QE/QT policies.