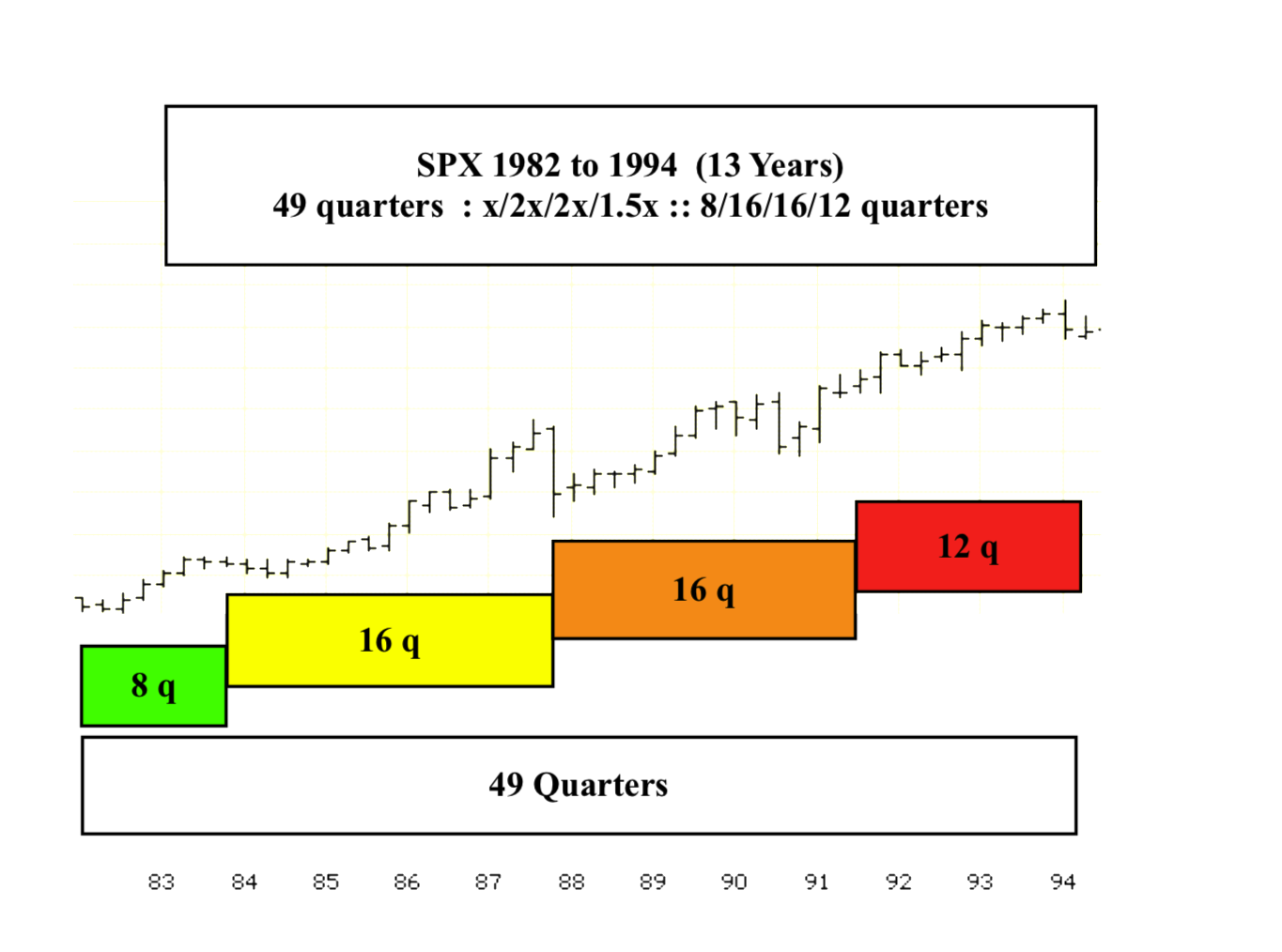

Fractal self-assembly and self ordering of asset valuations, traded daily (or five times a week), occur in combinations of three and four phase mathematical fractal series: x/2-2.5x/2-2.5x/1.5-1.6x and x/2-2.5x/1.5x-2.5x, where x denote a fractal time unit in days, weeks, months, and years.

An alternative 149-150 day DAX 17 January 2024 second fractal decay model of the 23 October 2023 60/125 day of 126 to 150 day first and second fractal series has no flash crash, rather a 14 July 2024 6/12/9-10 day :: x/2x/1.5-1.6x decay series ending 15-16 August 2024.

The current model for the DAX and western equity composites from the March 2020 covid low is an averaged 8-9/23-24/23/1 of 12-15 month :: x/2.5x/2.5x/1.4-1.6x four phase growth and decay fractal series.

The expected June- Sept 2025 low for global equities represents the end of a major consumer-citizen 1982 13/32-33 year debt-dependent credit cycle, where asset prices in the terminal 32nd/33rd year of he second fractal particularly, global residential asset and equity prices will fall precipitously and debt default and restructuring will occur, forming the basis for another 30-33 year inflationary credit expansion.

The expected incipient August September 2024 Fed fund rate cuts and mid August 2024 149-150 day second fractal nadir valuation saturation selling would provide two explanations for rebound valuation growth beyond the incidental US November 2024 election cycle.