Oil’s Deep Dive: Is the Asset Debt Macroeconomic System Quantitative and Deterministic? 17 December 2015 Gary Lammert Leave a comment

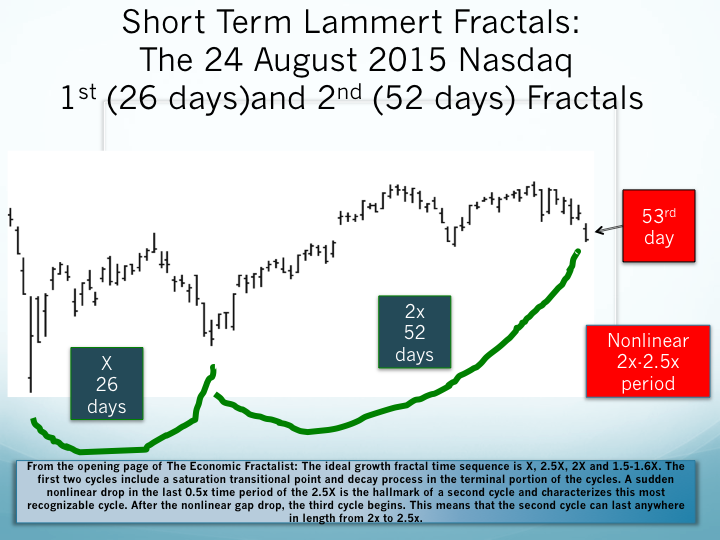

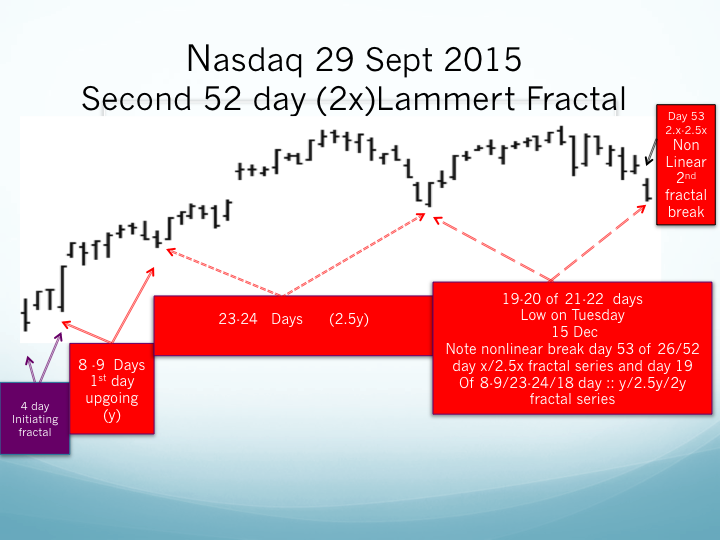

Small Scale and Large Scale (Short Term and Long Term ) Lammert Fractals : The Asset Debt Macroeconomic System 13 December 2015 Gary Lammert Leave a comment CRB 2015