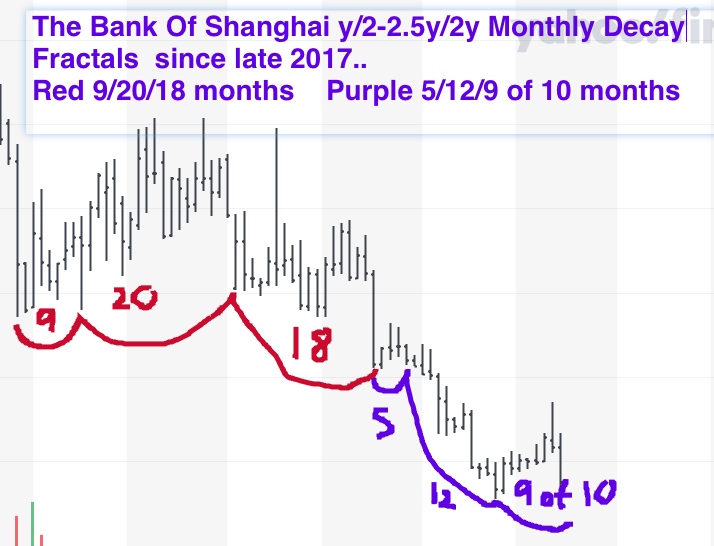

The Debt Market Side of the Asset-Debt Macroeconomic System: Now 8 days to a Historical 1982 13/30 Year First and Second Fractal Equity and Commodity Asset Valuation Nonlinear Low

The global central banks’ manipulable debt markets represent both an accelerator and conversely the boron rods of a potentially exponential fissionable asset over production and price over valuation.Lowering and raising of interest rates represent boron rod withdrawal and insertion, respectively equating broadly to QE and QT..

At persistently zero or negative interest rates, there is no limit to asset over production and valuation. The result is hyperinflation and the resulting complete dissolution of the socialcontract for workers and pensioners, the stuff that maintains the macroeconomic system’s equilibrium. At high borrowing rates, the boron rod effect collapses growth activity, resulting in decreased economic activityand unemployment. If extreme., these boron rods can implode the system.

The March 2020 Ten Year Note weekly fractal sequence is 30/75/72 of 74 weeks. The 72 of 74 week third fractal is composed of a 4/10/10 week series followed by a 8/19/17/10 of 12 week series. The final 4th fractal 12 week series of the latter weekly series starts on 5/11/2023 and is composed of a 8/19/18/5 of 13 day sequence. The next 8 trading days could reasonably complete a 1981-82 13/30 year first and second fractal series, interpolated within the US hegemony 1807 36/90/90/54 year series with its 90 year third fractal (composite equity and crypto) asset valuation peak on 8 November 2021. Historical second fractal terminal 2x-2.5x area (26- 32 year) nonlinearity would result in both sudden and huge declines in equity and commodity valuation prices.

Expect the unexpected. Over the next 8 trading days, money exiting commodities, equities, and crypto will flow into US debt instruments driving US debt interest rates much lower.

The Fed may lower interest rates at the 25-26 July 2023 meeting simply to keep their policy in tune with US debt instrument actual market forces and a sudden drop in commodity and equity prices.