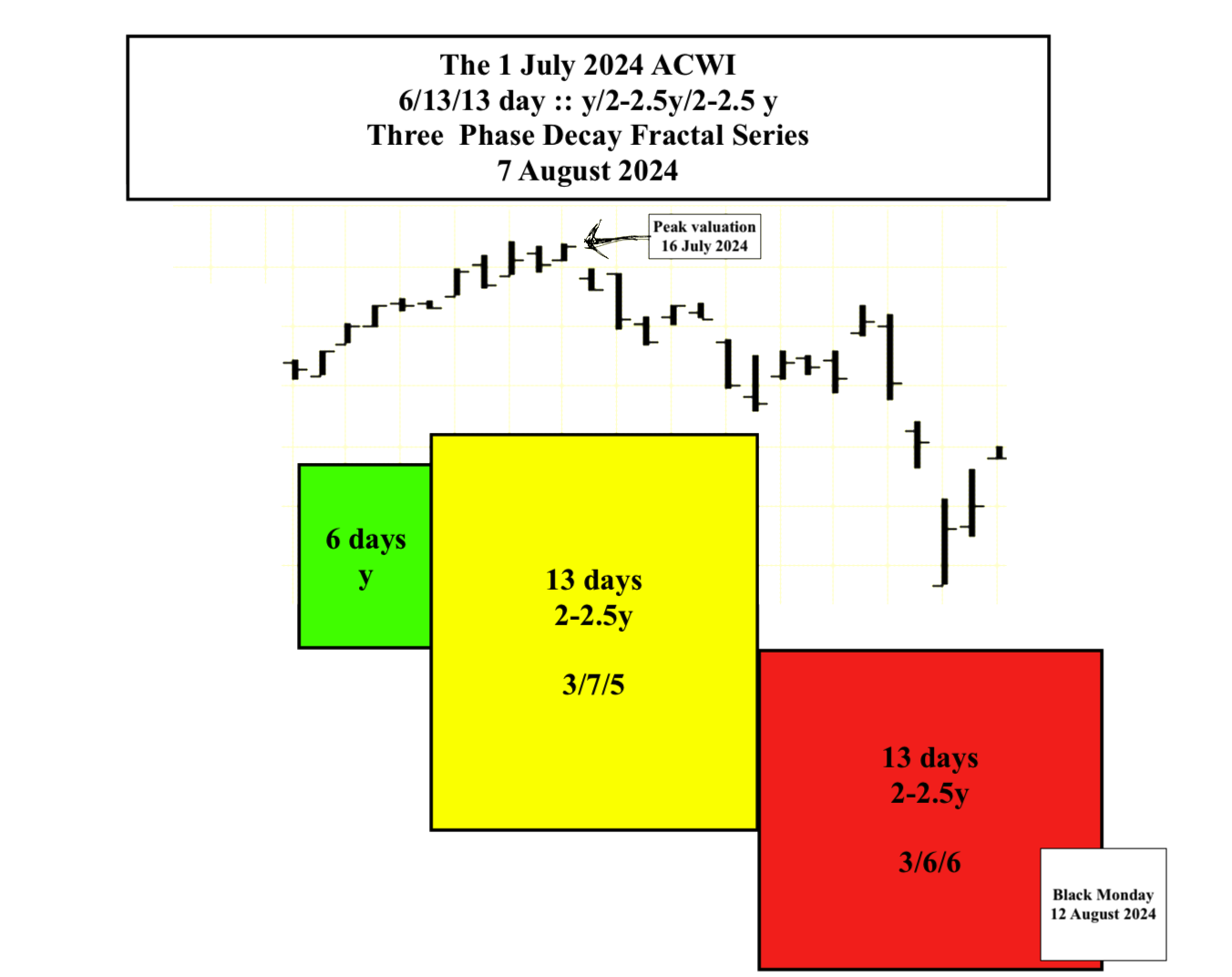

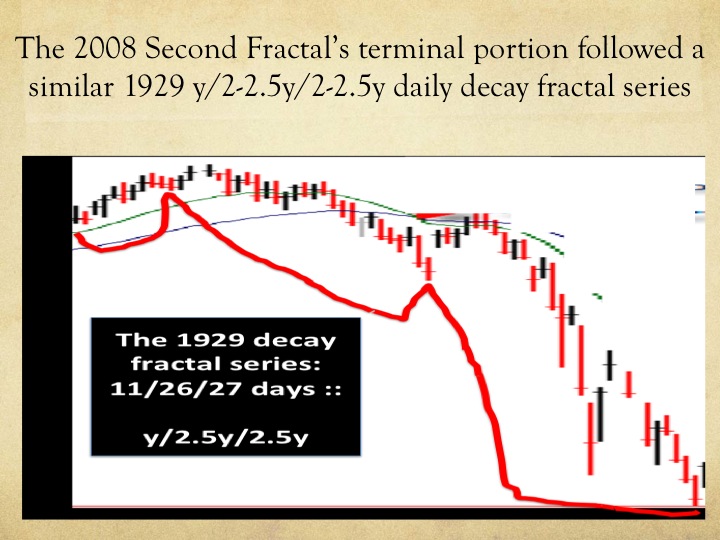

12 August 2024 will complete an incipient 1 July 2024 6/13/13 day :: y/2-2.5y/2-2.5y three-phase fractal decay series containing the 16 July 2024 peak valuation day , analogous to 1929’s incipient 11/26/27 day :: y/2.5y/2.5y three-phase decay fractal series also containing the peak valuation day.

The 1982 to 2025 13/32 year :: x/2.5x first and second fractal series is a fractal replay of 1807 to 1932 36/90 year :: x/2.5x fractal series and an interpolated large scale fractal series within the larger 1807 36/90/90/54 year :: x/2.5x/2.5x/1.5x series ending in 2074.

Is the asset debt macroeconomic system self ordering and deterministic? At the minimum this construct is an interesting, testable, and observable hypothesis.

The ACWI world composite, unadjusted for inflation, peaked in July 2024. The index is in the lineage of the US hegemonic 1807 36/90/90/54 year great x/2.5x/2.5x/1.5x Four Phase Fractal Series ending in 2074 with progenitor nadir valuations in 1842-43, 1932 and with an inflation adjusted 90 year third fractal peak in November 2021.

From 1932 US equities followed a 10-11/21-22/21-22 year fractal series :: x/2x/2x ending in 1982 ending with high Volcker QT fed fund rates that have since cascaded lower and lower and post the 2009 global housing bubble collapsed to near zero.

Low inflation during this low interest rate period was facilitated by imported low cost manufactured goods from China, use of natural gas as an energy source, and fracking which elevated US oil production and export to levels not seen in decades. During covid, historically large % GDP deficit spending, 2.5-3% mortgage rates, supply line disruptions, and corrupt corporate price fixing produced a 10% inflation rate. In response the US central bank invoked Volcker-like QT with an inversion of short term -long term bond yields that has lasted more than 600 days, longer than the inversion leading up to the 1929 crash.

The observed fractal series since 1982 is 13/31 of 32 years with an expected large scale 2024-2025 second fractal crash. (See main page of the Economic Fractalist). This is part of a 13/32/32-33/20 year :: x/2.5x/2.5x/1.5 x interpolated fractal series ending in 2074. The third 32-33 year fractal starting in 2025 will see the greatest monetization of national debt and social contract liabilities in world history.

The yearly fractal series groupings since 1982 can be observed using the SPX. The first 13 year fractal is composed of a 3/7/5 year series ending in 1994. The second fractal is composed of two series: 3/7/7 years and 4/8/7 of 8 years ending in 2025.

The terminal portion of the 1994 current 31 year second began in March 2020 and follows a 8-9/24/23 month :: x/2.5x/2.5x fractal growth sequence peaking(unadjusted for inflation) in July 2024(July 6 to be exact). The 23 month third fractal of the 8-9/24/23 month series is composed of a 5/10/10 month series. The third 10 month series started in October 2023 and is composed of a 13/28 of 31-33 week :: 59-60/149-150 day series expected to end on about 12 August 2024. This is the incipient 13/31 of 32 year 1982 31-32 year second fractal crash.

The final nonlinear daily decay appears to be a 7-/13/13 day fractal :: y/2y/2y ending 12 August 2024 with a possible lower low extension of 8-9 days (y/2y/2y/1.5y’). Will the August 12 2024 low and the possible extension low be below the Oct 2023 low? During the next 8 trading days ten year notes will trend significantly lower …

(Added 28 July 2024 : two alternative mathematical crash fractal models have been added below on 27 July and 28 July 2024-see below)

The ACWI world composite, unadjusted for inflation, peaked in July 2024. The index is in the lineage of the US hegemonic 1807 36/90/90/54 year great x/2.5x/2.5x/1.5x four phase Fractal Series ending in 2074 with progenitor nadir valuations in 1842-43, 1932 and with an inflation adjusted peak in 2021.

From 1932 US equities followed a 10-11/21-22/21-22 year fractal series :: x/2x//2x ending in 1982 with high Volcker QT fed fund rates that have since cascaded lower and lower and post the 2009 global housing bubble have collapsed to near zero.

Low inflation during this low interest rate period was facilitated by imported low cost manufactured goods from China, use of natural gas as an energy source, and fracking which elevated US oil production and export to levels not seen in decades. During Covid large % GDP deficit spending, 2.5-3% mortgage rates, supply line disruptions, and corrupt corporate price fixing produced a 10% inflation rate. In response the US central bank invoked Volcker-like QT with an inversion of short term -long term bond yields that has lasted more than 600 days, longer than the inversion leading up to the 1929 crash.

The observed fractal series since 1982 is 13/31 of 32 years with an expected large scale 2024-2025 second fractal crash. (See main page of the Economic Fractalist). This is part of a 13/32/32-33/20 year :: x/2.5x/2.5x/1.5 x series ending in 2074. The third 32-33 year fractal starting in 2025 will see the greatest monetization of national debt and social contract liabilities in world histor.

The yearly fractal series groupings since 1982 can be observed using the SPX. The first 13 year fractal is composed of a 3/7/5 year series ending in 1994. The second fractal is composed of two series: 3/7/7 years and 4/8/7 of 8 years ending in 2025.

The terminal portion of the 1994 current 31 year second began in March 2020 and follows a 8-9/24/23 month :: x/2.5x/2.5x fractal growth sequence peaking(unadjusted for inflation) in July 2024. The 23 month third fractal of the 8-9/24/23 month series is composed of a 5/10/10 month series. The third 10 month series started in October 2023 and is composed of a 13/28 0f 32 week :: 59-60/149-150 day series expected to end on about 16 August 2024. This is the incipient 13/31 of 32 year 1982 31-32 year second fractal crash.

A Comparison of the underperforming French CAC,(now below its recent 6 month average)with the better performing world composite ACWI which contain US, Japanese, and Indian stocks is useful in defining the final daily fractal decay series which appears for the ACWI to have started on 28 June 2024 and is composed of a 7/13 of 16-18/14 day :: y/2-2.5y/2y series ending on 16 to 20 August 2024. Like the 11/26/28 day :: y/2.5y/2.5y decay series occurring in 1929, a significant rebound of global equities is expected to occur beyond the early November 2024 US presidential elections.

Added 27 July 2024:

An alternative crash fractal pathway ending 20 August 2024 is observable: a 28 June 224 3/7/6 day growth pattern which peaks on the day 2,3, and 4 of the final 11 July 6 day third fractal and ends lower with a valuation lower than day 1 of the 6 day fractal series . This 11 July 2024 6 day sequence of final growth and decay becomes the first base fractal for a 11 July 6/12/12 day :: y/2y/2y crash decay fractal series ending 20 August with possible y/2-2.5y/1.5-2.5y decay fractal variations.

Added 28 July 2024

A third alternative for a quantitive mathematical fractal blow-off growth from 28 June 2024 for the World Equity Index ACWI is a 4 phase fractal blow-off series from 28 June 2024 of 2.5/5/5/4 days :: x/2x/2x/1.5x. The final 4 day 4th fractal in this series starts on 15 Jul2024 and contains the all time ending peak valuation on 16 July 2024.

This 15 July 4 day 4th fractal in the 28 June 2.5/5/5/4 day 4 phase series become the base for a 4/10/10 days :: y/2.5y/2.5y crash series ending 13 August with a possible lower low extension of 6 days 4/10/10/6 days :: y/2.5y/2.5y/1.5y ending on 20 August 2024.