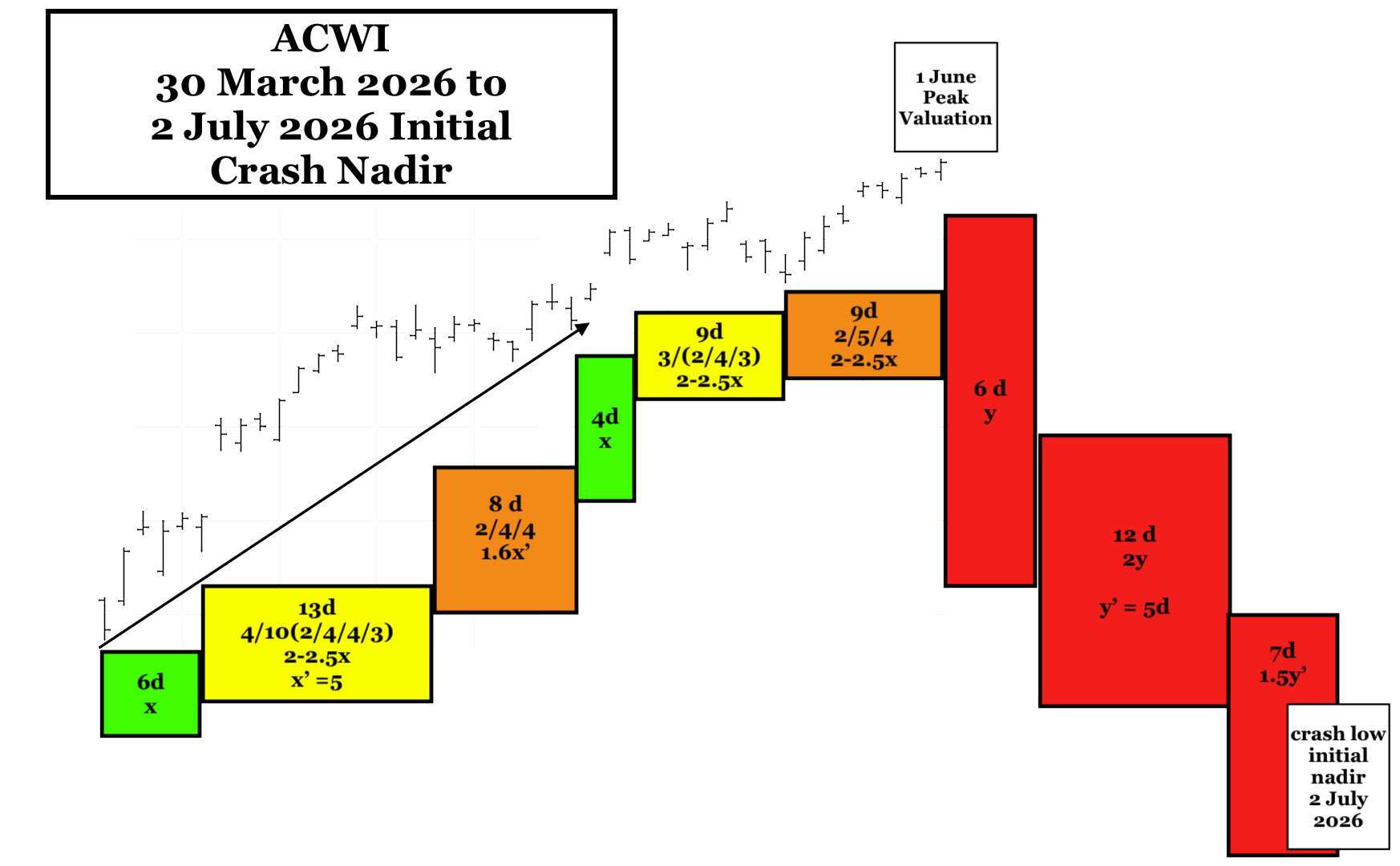

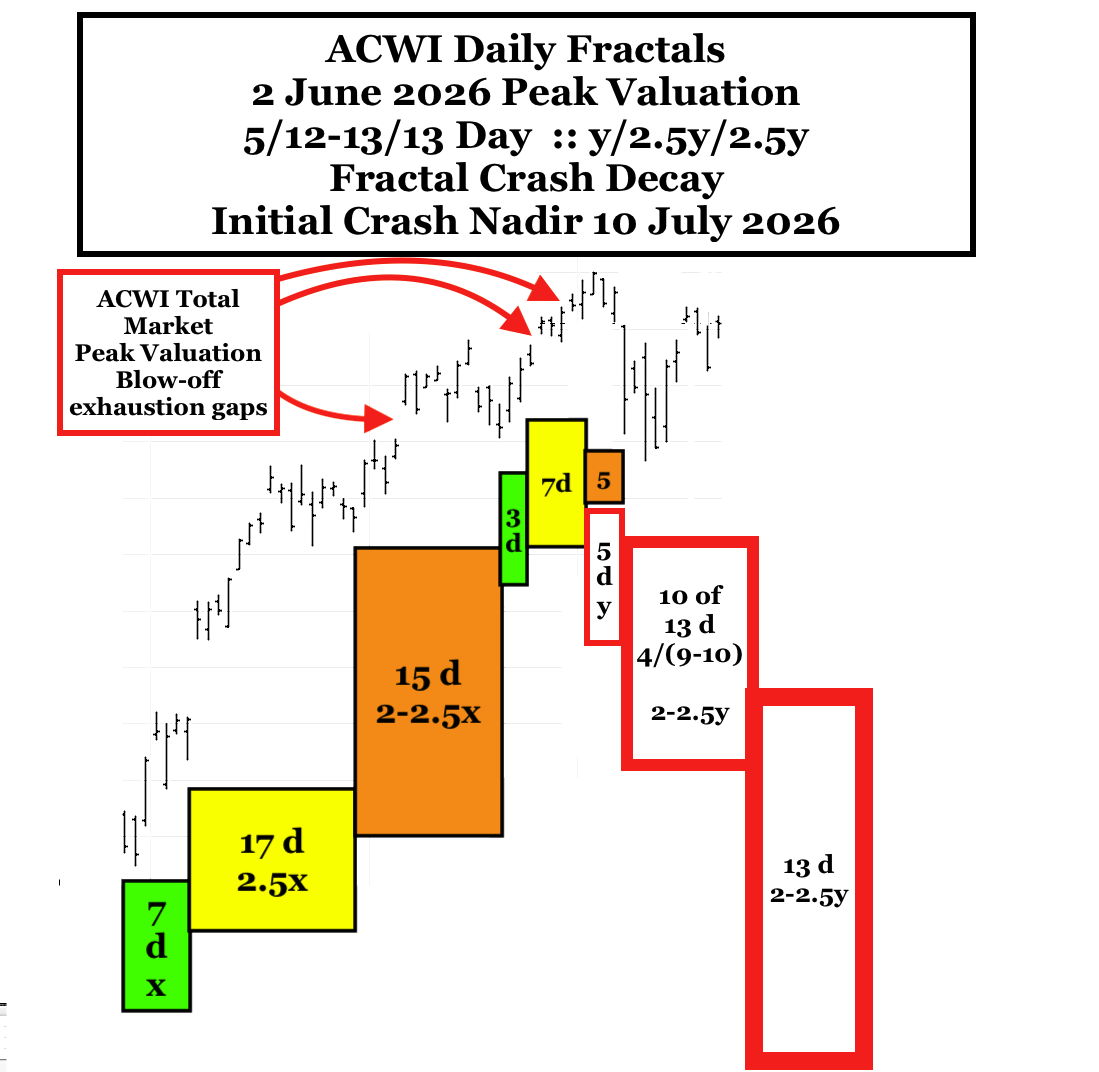

Three exhaustion gap opening day valuations to new all-time peak valuations

occurred since 5 May 2026, technically indicating terminal valuation growth with final peak valuation on 2 June 2026. 2 June occurred on the 2nd day of a 5 day 3rd fractal of a 19 May 2026 3/7/5 day :: x/2-2.5x/1.6x day terminal 3-phase fractal series. The terminal 5-day 3rd fractal became the base 1st fractal for a 5/12-13/12-13 day :: y/2.5y/2.5y 3-phase Lammert Crash Decay series with an initial crash nadir ending on 10 July 2026.

Global corporate and private monthly/yearly debt obligations coupled with current interest rates are at GDP ratio highs. US malinvestment into AI and Space X are at blow-off frothy highs. Private debt corporations are restricting disinvestment schedules. 20% and 50% declines in gold and crypto currency from peak valuations serve as seismic activity directional indicators of global liquidity problems underlying the fragility of all asset valuations within the asset-debt system. US consumer sentiment, promoting 70% of the US economy, is near an all time low, buoyed last month by falling gas prices secondary to the massive release of oil from the strategic reserves.

2 June 2026 was the 33 year 2nd fractal ACWI and SPX valuation peak of a 1982 13/33 year :: x/2.5x 1st and 2nd fractal series interpolated within an 1807 to 2074-2077 US hegemonic asset-debt macroeconomc 36/90/90/54-57 year : x/2.5x.2.5x/1.5-1.6x 4-phase Lammert fractal series.