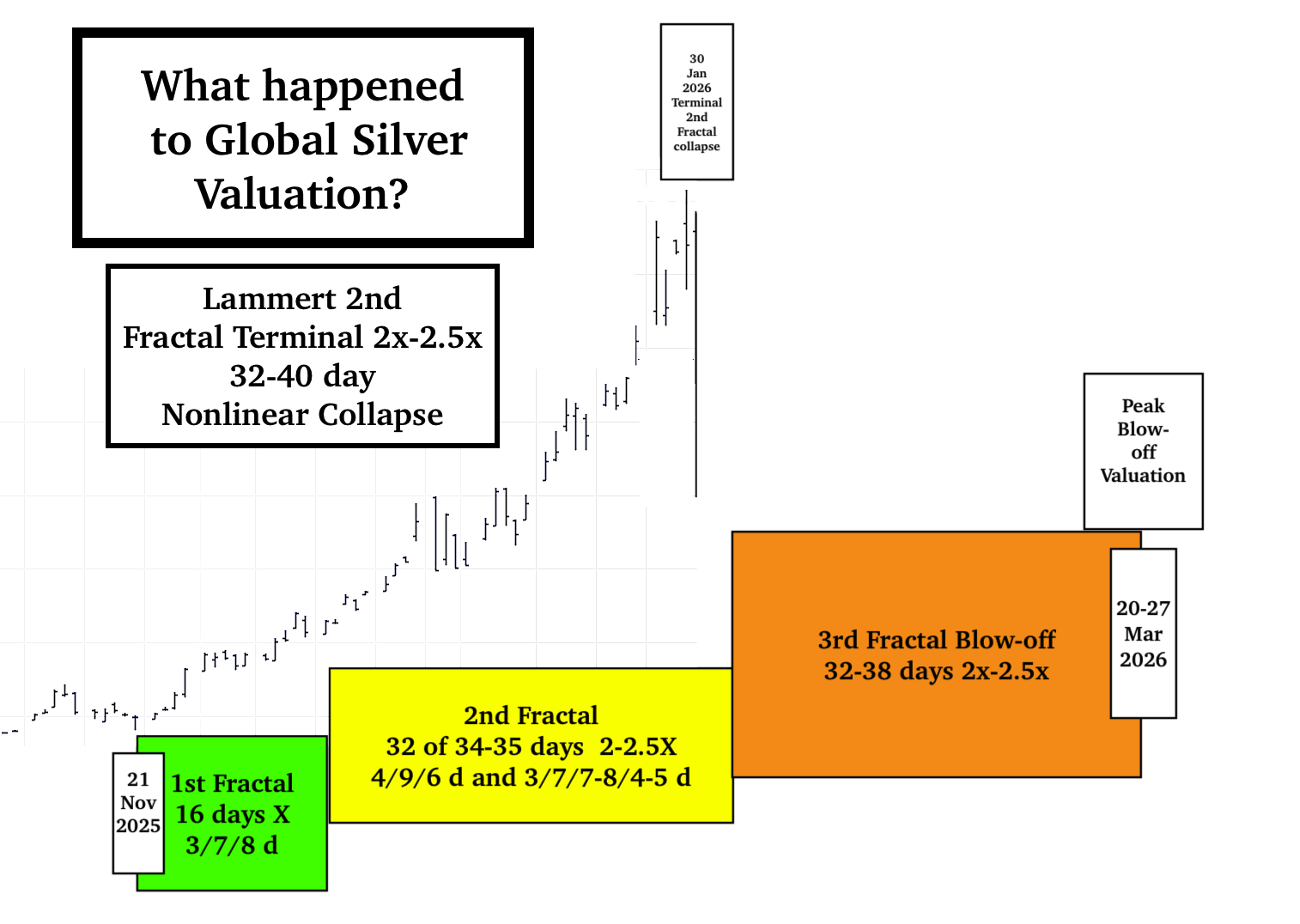

The flash crash on 6 May 2010 was representative of Lammert 2nd Fractal nonlinearity with a daily composite equity loss of nearly 10%. Silver’s flash crash of 30 Jan 2026 represented a 31.37% drop … again a result of Lammert Saturation Asset-Debt Fractal Macroeconomics and Lammert 2nd Fractal Nonlinearity …

The blow-off valuation in gold and silver in US dollars ending 20-27 March 2026 will be unparalleled.

The antiinstitutional, anti-alliance, anti-domestic law, anti-international law, anti-free trade, gross overt international and domestic corruptional … grossly lawless and plainly idiotic policies – facilitated by the majority US supreme court members – by the current American government has obliterated faith in American consistency and global leadership. The world’s preference for the traditional choice assets of value, gold and silver, will result in an historical valuation blow-off of these assets with a peak valuation between 20-27 March 2026.

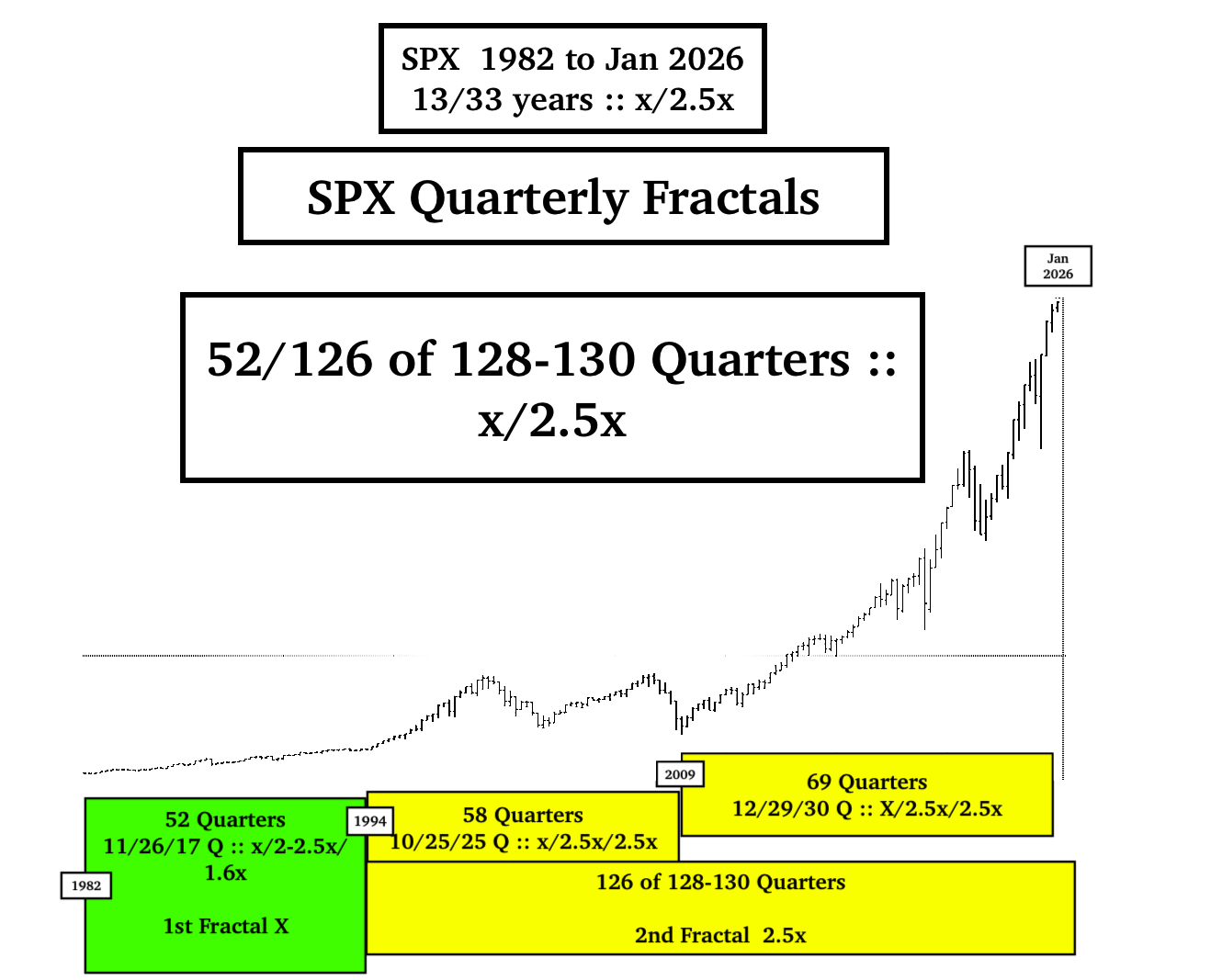

While there will be counter valuation growth cycle after the 27 March 2026 ACWI Global Equity Valuation Peak, the 1982-2026 13/33 year :: x/2.5x 1st and 2nd fractal global equity crash will occur over a relatively short time frame.

A Primer on Quantitative Time-based Self-Assembly Lammert Fractal Growth and Decay of Valuations of The Asset-Debt Macroeconomic System’s Composite Equities

Qualitatively …on the longest time-unit cycles (years) (e.g. 1807 36/90/90/54-57 years :: x/2.5x/2.5x/1.5-1.6x and 1982 13/32 of 33/32-33/20 years x/2.5x/2.5x/1.5-1.6x) credit expands via governmental, corporate, and citizen debt; assets are produced and over-produced , overvalued and over-consumed; consumers reach maximum debt loads; the population of possible traders/invested are fully invested and composite equity asset valuations reach a singular fractal time-unit (minute, hour, day, week, month) peak valuation and thereafter undergo decay; recessions occur with weakening demand, interest rates fall; excess debt undergoes default and restructuring; individual and corporate bankruptcies occur; and composite equity (and commodity) asset valuations eventually reach a singular fractal time-unit nadir. The cycle thereafter repeats itself.

On smaller time-unit fractal cycles (quarters, months, weeks, days, hours, 15-minute/ 5 and 1-minute) : trader/investor population saturation of asset buying occurs ending in a transient peak valuation .. followed by trader/investor population saturation end selling resulting in a transient nadir valuation. These peaks and nadirs occur in one of the two quantitative fractal patterns as above.

Empirically composite equity asset valuation growth and decay cycles occur in 2 modes(laws) of mathematical deterministic self-organizing, self-assembly time-based fractal series:

a 4-phase fractal series: x/2-2.5x/2-2.5x/1.5-1.6x and a 3-phase fractal series: x/2-2.5x/1.5-2.5x

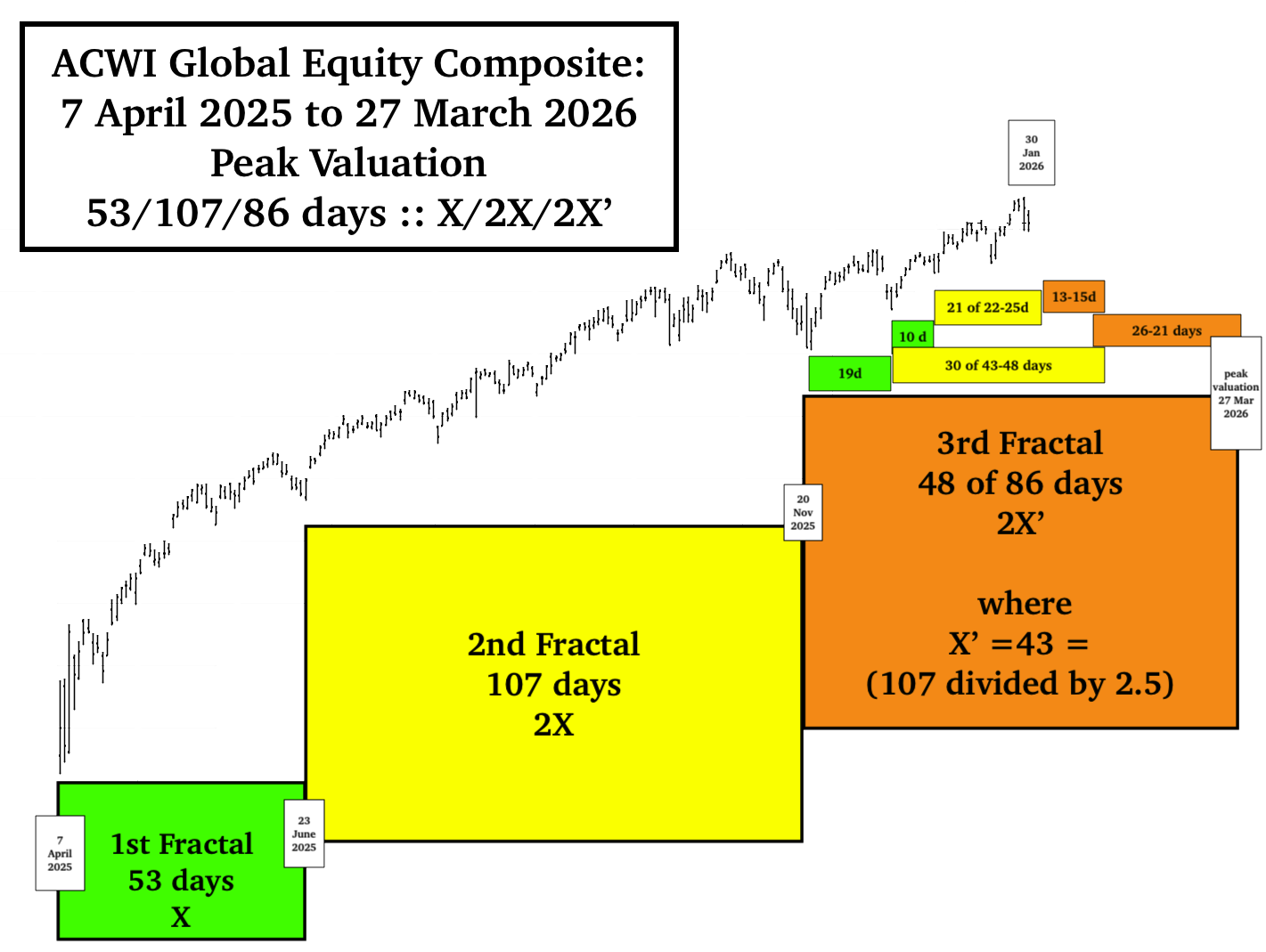

In the 4-phase fractal series sequential elements are termed: the 1st, 2nd, 3rd, and 4th fractals and in the 3-phase fractal series: the 1st, 2nd, and 3rd fractals.

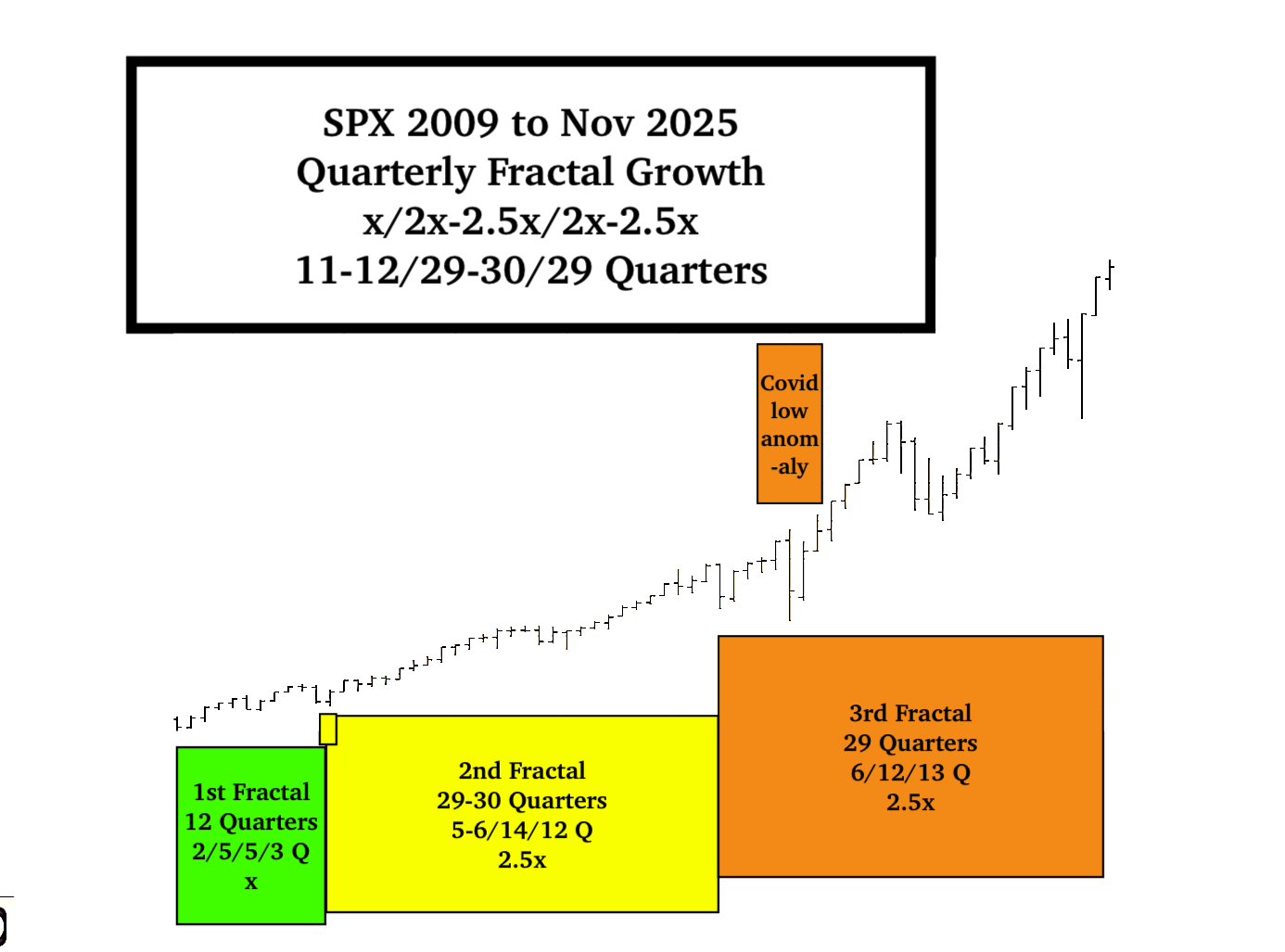

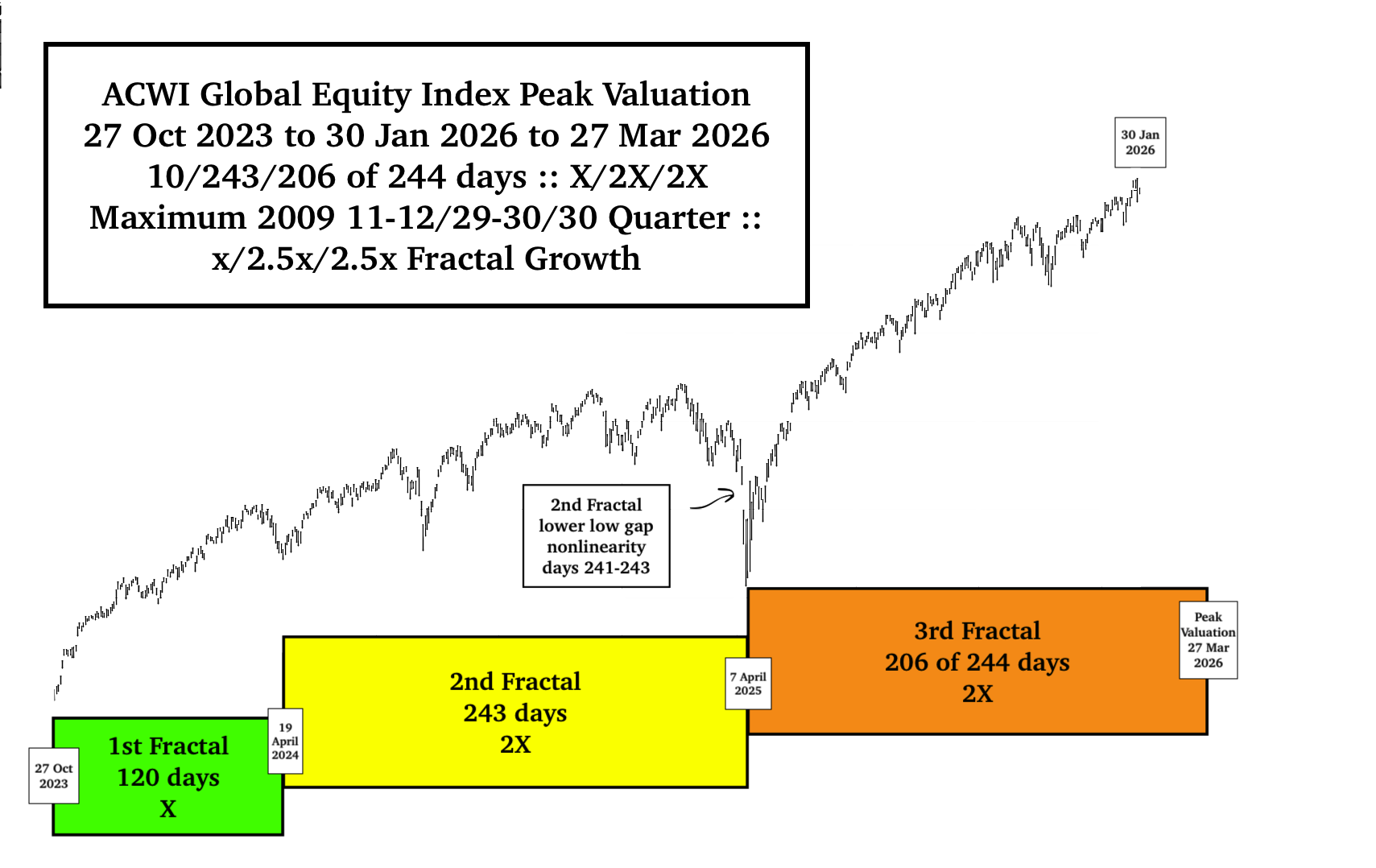

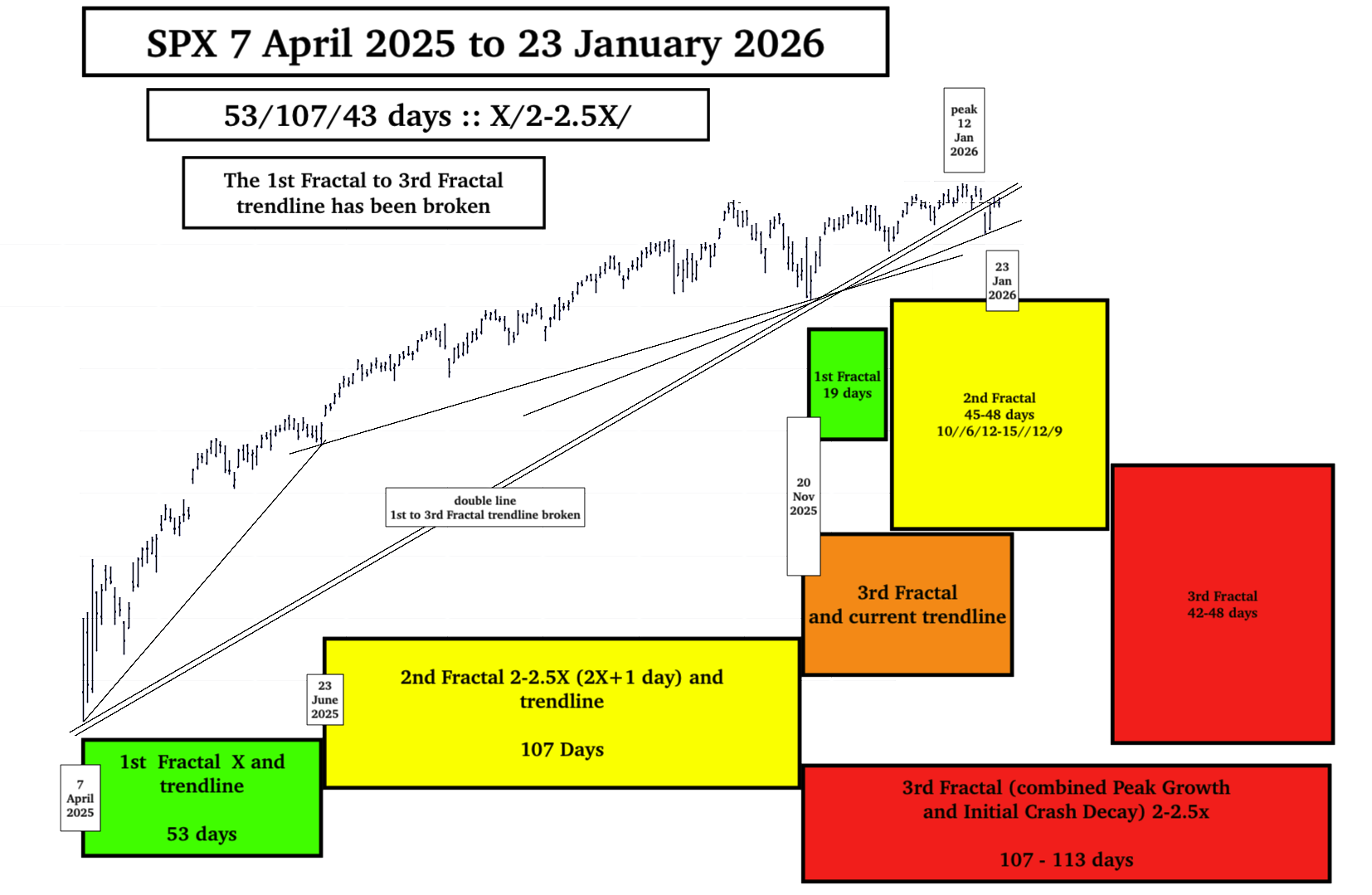

The 2nd fractal is characterized by terminal gapped nonlinear lower lows between the 2nd fractal’s terminal 2x and 2.5x time period. (These gapped nonlinear lower lows can be observed in weekly valuation units for the DJIA between 1929 and 1932, the terminal portion of the US 90 year 2nd fractal; within the last three day before the terminal 5 August 2024 139 day 2nd fractal low occurring in an interpolated ACWI/SPX 27 October 2023 55/139/135-136 day (SPX-ACWI respectively) :: x/2.5x/2.5x valuation maximum growth series ending 18/19 February 2025: and can be expected within the last months on a daily and weekly basis of the current 32 of 33 year 2nd fractal of the interpolated 1982 13/32 of 33 year 1st and 2nd fractal series. (The 27 October 2023 dominant fractal series appears to have a 119 first fractal base, whereas the 55/139/136 day 3 phase growth series was a secondary interpolated series).

With the exception of the 3rd fractal in the 4-phase series whose fractal grouping is determined by its terminal high or final lower high peak valuation, fractals (fractal groupings) are determined by the nadirs of the first and last time unit in the grouping with all intervening valuations above the connecting nadir trend-line.

In the asset-debt macroeconomic system, expansion of credit and a growing money supply – occur primarily via US sovereign or other sovereign directed debt markets. This constant credit expansion is essential for the ongoing liquidity needed to support higher equity valuations. Sovereign debt expansion follows governmental fiscal deficit spending and its expansion.

When the system’s lender participants demand higher sovereign debt interest rates primarily because of the higher risks associated with grossly peak overvaluation of equities, real estate, and commodities and concerns about fiscal responsibility, the asset debt system reaches an inflection point; and non-debt asset valuations nonlinearly devolve to new price levels reflecting the default, liquidation, and/or reordering of non-repayable private debt in the real economy, i.e, corporations and individuals.

With the Nikkei’s and the Wilshire’s close to 210% of GDP valuations, it appears that the global sovereign global debt market is very near that inflection point. Added to the overvaluation of equity relative to GDP is the anti-institutionalism and anti-constitutionalism of the current administration’s American trade and alliance mutable transactional policies and divergence from the traditional domestic rule of law policies.

Current 7 April 2025 to 23 Jan 2026 SPX growth and initial crash decay fractal model.