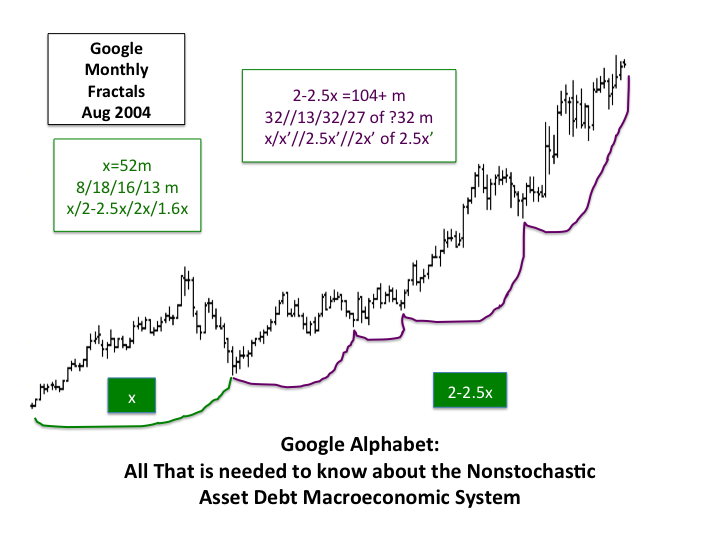

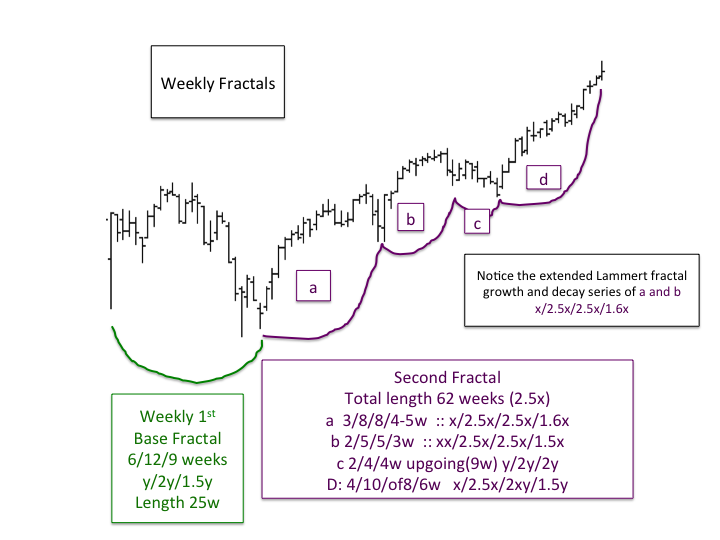

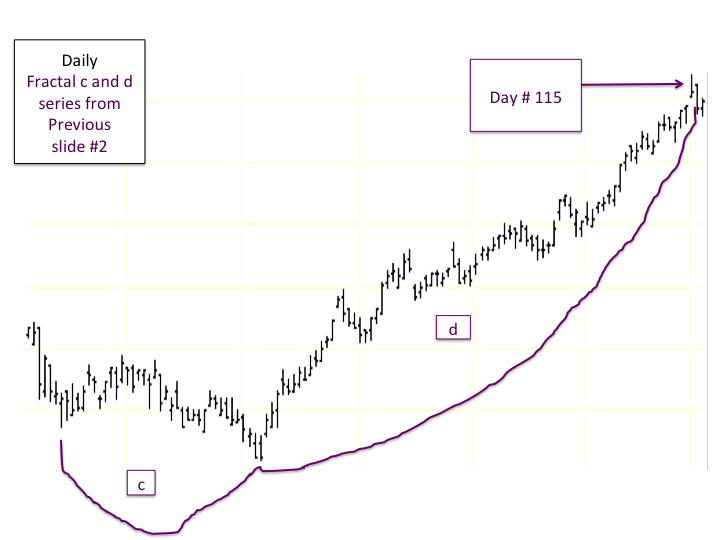

The Elegantly Simple Self-Assembly Deterministic Growth and Decay Of the Asset Debt Macroeconomic System: Alphabet Google is All That is Needed to Confirm the Structure 5 March 2017 Gary Lammert 1 Comment

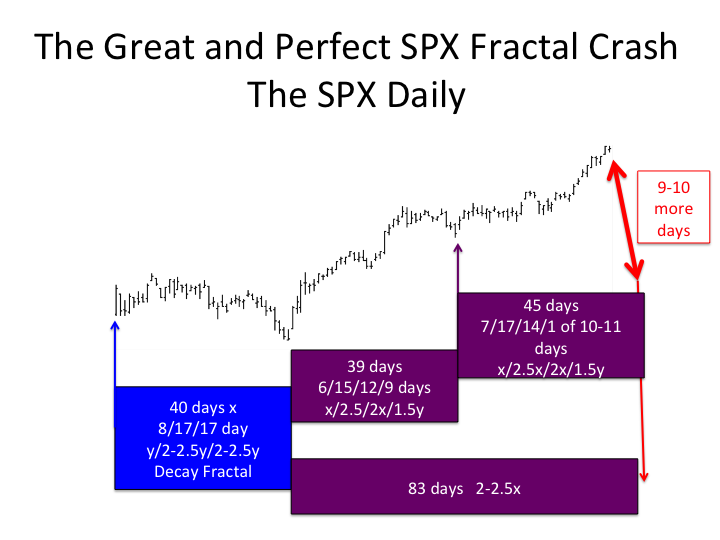

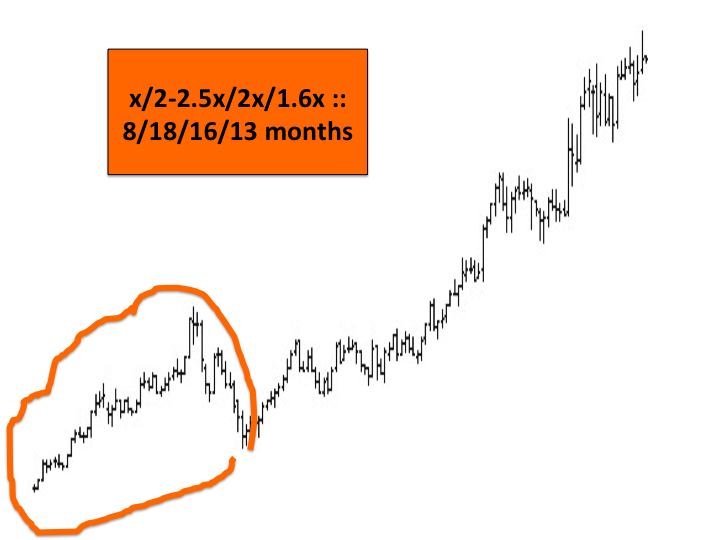

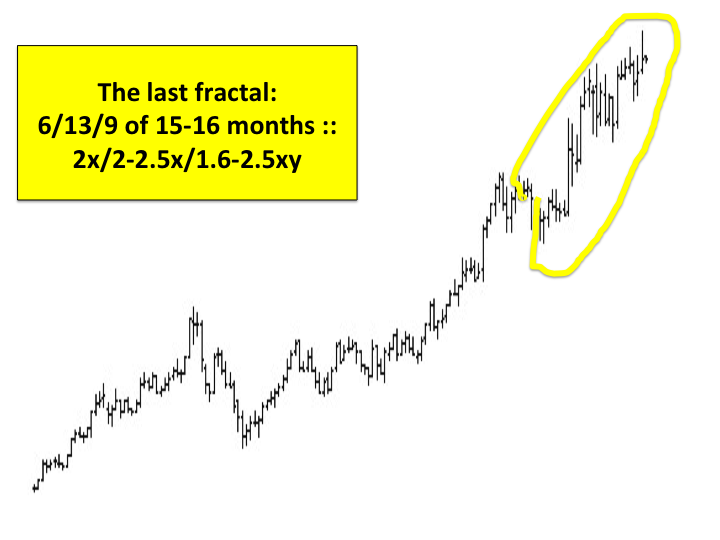

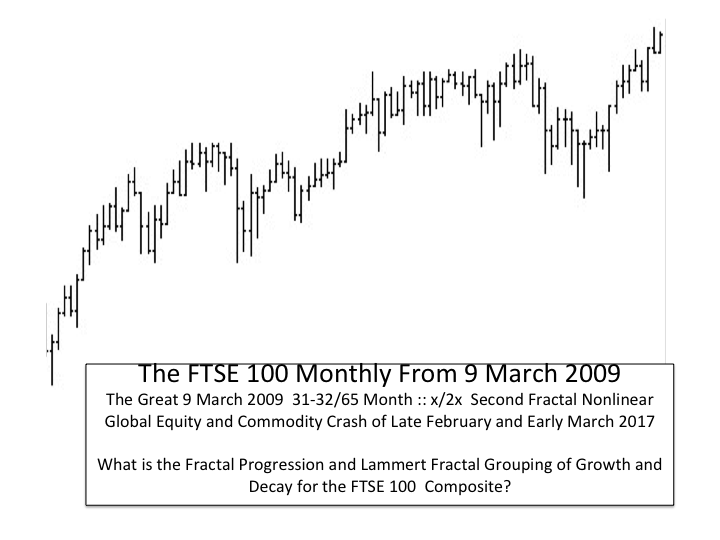

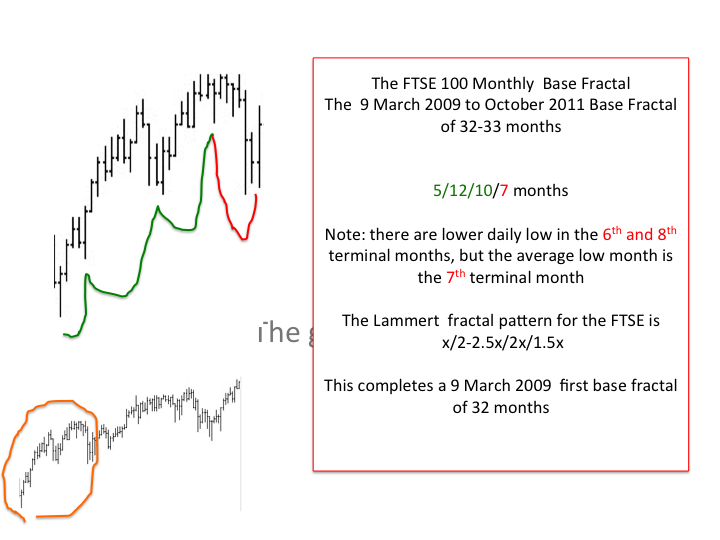

Not Smart At All: Poor Pattern Recognition Cognition: The Great 9 March 2009 2nd Fractal Crash: SPX Daily, Google Monthly, FTSE100 Monthly 23 February 2017 Gary Lammert 2 Comments This is the ubiquitous Lammert Growth and Decay Pattern which accompanies the x/2.5x/2.5x/1.5-1.6y pattern, the y/2-2.5y/2-2.5y decay pattern and the x/2-2.5x/1.5-1.6x basing pattern …

Hangseng Composite and Silver in US dollars :: 5/10/10/1 of 7-8 days:: x/2x/2x/1.5-1.6y 30 January 2017 Gary Lammert Leave a comment