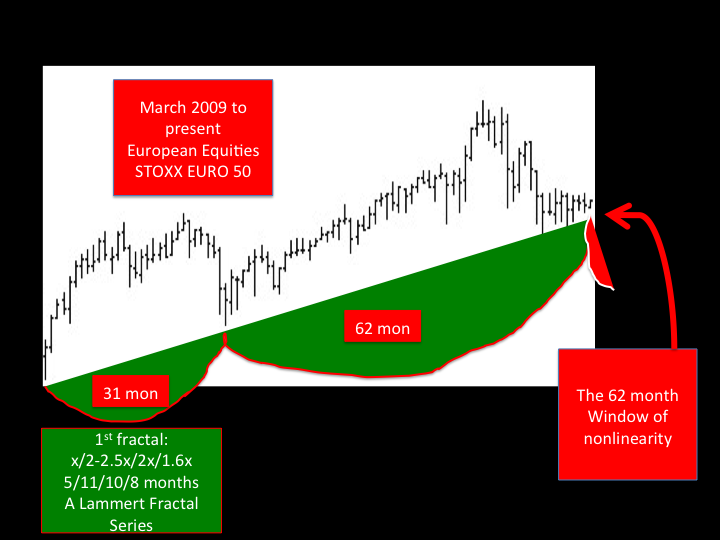

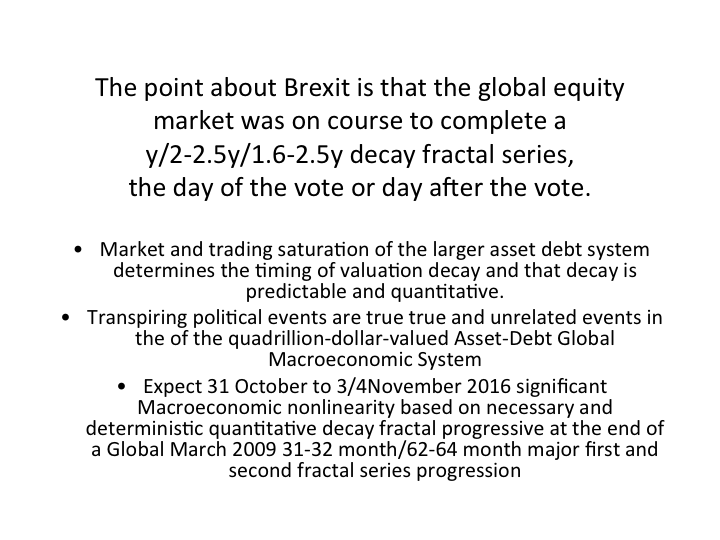

31/62 Month :: x/2x Global Equity Second Fractal Nonlinearity: Both the British Brexit Vote and the US Political Turmoil Have No Effect On the Deterministic Fractal Evolution Of the Quadrillion Dollar Equivalent Asset Debt Macroeconomic System

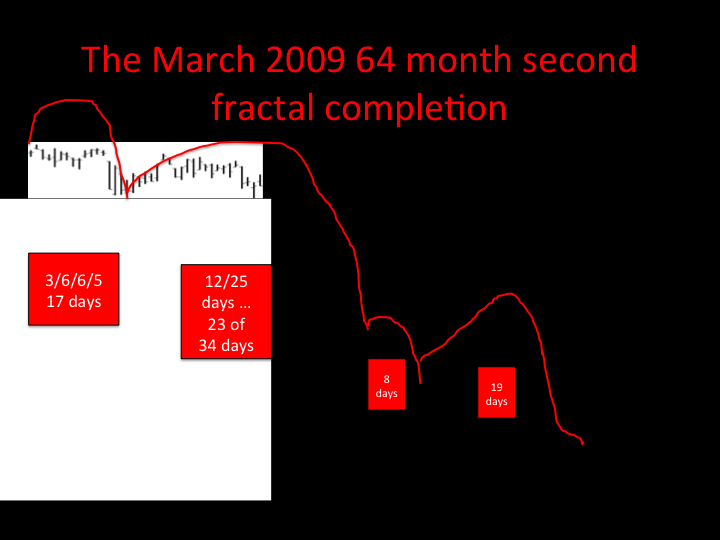

The March 2009 64 Month global Equity Second Fractal Terminus